SpaceX’s blockbuster bond sale is weakening so quickly in the secondary market that traders say they can’t recall another recent deal that widened this sharply.

One large dealer was quoting SpaceX bonds maturing in 2056 at levels as much as 0.28 percentage point wider than the issue price of 1.75 percentage points above Treasuries, according to people with knowledge of the matter, who asked not to be identified discussing private activity in the over-the-counter market.

Paper losses on SpaceX’s $25 billion offering have mounted since the debt began trading and totaled roughly $305 million as of late Thursday relative to Treasuries. The longest-dated SpaceX bonds, which drew more skepticism than those with shorter maturities, have effectively erased all the tightening from underwriters that followed as orders swelled to nearly $90 billion.

Traders say the moves suggest fast-money accounts, rather than traditional buy-and-hold investors, piled into the deal looking to flip it for a quick profit. The selling pressure stands out even more because SpaceX shares have been largely stable since the bonds priced on Tuesday, after lurching 16% lower the day before.

Even if there are more technical reasons behind the selling — hedge funds covering or hedging short positions, for example — the virtually unprecedented magnitude points to SpaceX’s unique profile. The company, which at its peak this month had a $2.64 trillion market value, won investment grades despite expectations for years of negative cash flow and a dependence on Elon Musk that Fitch Ratings deemed a “key rating constraint.”

“We expected SpaceX to widen from issuance level, but not this much,” said Tony Trzcinka, a portfolio manager at Impax Asset Management. “That magnitude is likely a perfect storm of the stock shedding $600 billion+ since launch, weak technicals from the upsized supply, and investors still scratching their heads over how to price its unique risk profile.”

It’s a rare spread move when compared with how other recent mega bond sales have traded in the secondary market. Take Nvidia Corp., which raised $25 billion in a seven-part high-grade offering this month. The spreads on its 5.55% bonds maturing in 2046 have widened by 8 basis points since issuance, similar to the spreads on its 5.625% bonds maturing in 2056.

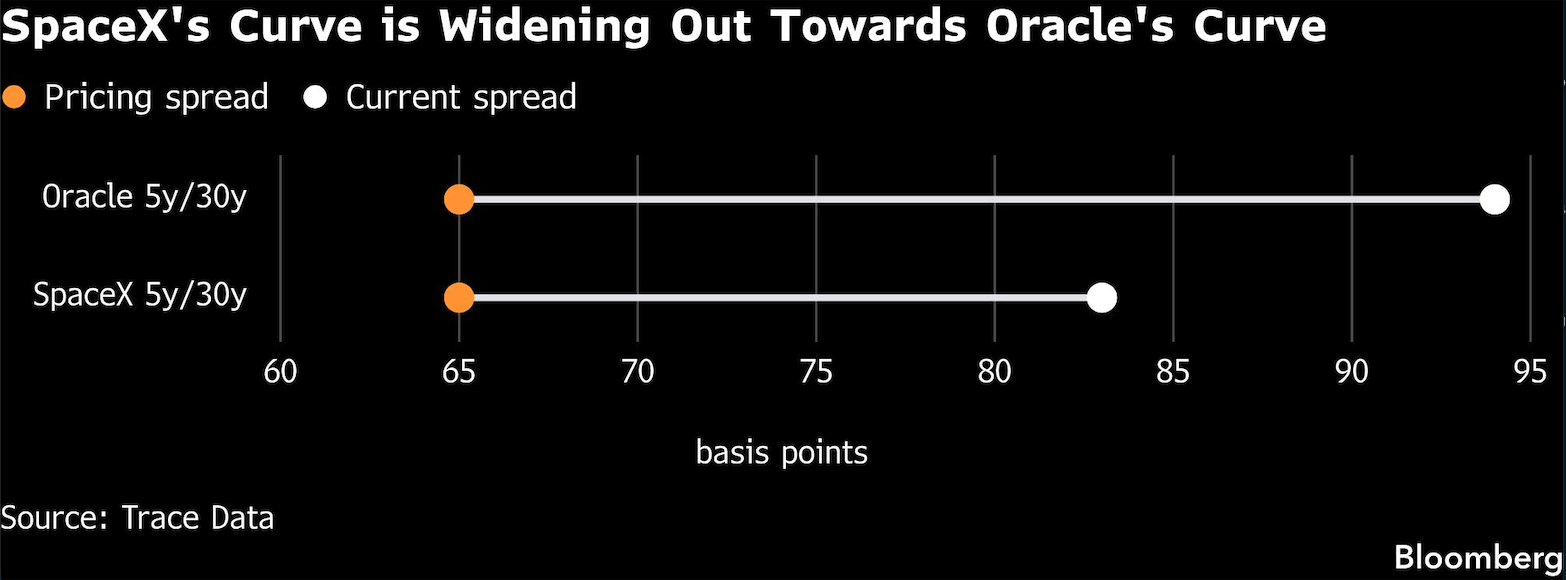

Meanwhile, risk premiums on Alphabet Inc.’s longer-dated bonds issued in February have tightened. Higher spreads typically signal that investors see a slightly higher chance of a company struggling to meet its obligations. After weakening, SpaceX’s credit curve is now trading more in line with those of similarly rated Oracle Corp., whose longer-dated bonds also widened soon after they were first sold.

Tech stocks dragged global indexes lower Friday following renewed selling in chipmakers, while a report that OpenAI could postpone plans to go public also weighed on sentiment. Two of China’s best-known hedge fund managers are warning that the artificial intelligence boom in global stock markets has become an unsustainable bubble.

Demand for the SpaceX bond sale was strongest for the five-year notes, which let the company cut borrowing costs more on that portion of the deal than on the longer maturities. Interest was weaker in the 20-year and 30-year bonds, which saw the biggest drop-off in demand.

A representative for SpaceX didn’t immediately respond to a request for comment, and the banks that managed the bond sale didn’t provide comment on SpaceX trading levels.

Bondholders have been inundated with mega bond sales this year as tech giants race to raise billions of dollars to finance artificial intelligence projects. US high-grade supply of $175 billion as of Tuesday has set a new June record, surpassing 2020’s $169 billion haul.

Credit-default swaps tied to SpaceX bonds began trading actively this week, Bloomberg reported on Thursday, allowing investors to hedge against potential losses or speculate on the firm’s creditworthiness. That creates more two-sided activity, or more ways to take exposure, which could boost trading in the bonds.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Caleb Mutua, Ying Luthra