It’s been a volatile few months for US debt and the dollar, with sudden shifts in trade and fiscal policy raising some concerns about the safe haven status of dollar-denominated assets. With US policy questions likely to remain front and center, we think bond investors wrestling with tariff-related volatility may want to lean into a more global approach.

We’re certainly not ready to call an end to the dollar’s preeminent role in the global economy. It remains the world’s most liquid currency, supported by the world’s deepest capital markets.

What’s more, there simply isn’t an obvious alternative to take the dollar’s place. Evidence of global reserve managers selling dollar-denominated Treasuries has been scarce too, though it’s possible some are hedging the dollar exposure that comes with those bonds. For investors who carefully manage their duration risk, we think dollar-denominated Treasuries will continue to stabilize portfolios in times of stress.

Policy Change: Dealing with the Unpredictable

But if there’s a gap in the dollar’s armor, we think it’s the increasingly unpredictable nature of US policy. The sheer scope of the tariffs that President Trump announced in April, for example, took markets by surprise; the policy twists and turns and temporary pauses since have intensified the sense of whiplash.

When Israeli air strikes on Iranian military and nuclear infrastructure began in mid-June—later supplemented by targeted US strikes—Treasuries initially rallied with gold. But yields rose shortly thereafter, partly due to concern about oil supply disruptions.

On the fiscal side of the ledger, the One Big Beautiful Bill Act is expected to increase the fiscal deficit by anywhere from $1.5 to $3 trillion over the next decade, with proposed tax cuts exceeding potential savings from cuts to clean-energy subsidies and Medicaid.

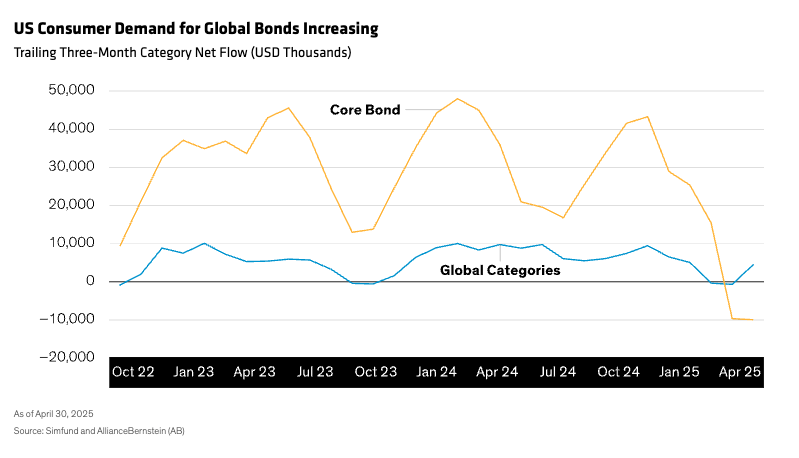

Going Global Could Boost Income and Trim Volatility

Investors worried about tariffs and wondering if US exceptionalism still holds may find opportunities in hedged global bonds. With a global fixed-income allocation, investors get access to a wider range of issuers, credit profiles and yield curves, which may add up to more income with less volatility.

What’s more, different countries operate under distinct economic, monetary and inflation regimes. For investors, those different paths may add up to less correlated return streams and alternative sources of income and risk. This may explain why recent data has shown signs that individual US investors have started to add exposure to global bonds (Display).

We believe that investors who globalize their bond portfolios today increase exposure to policies that lean into growth. That’s because many central banks around the world started cutting policy rates this year, prioritizing growth over efforts to push inflation back down to long-term targets. The European Central Bank has cut eight times in 2025, bringing the policy rate down to 2.15%. That’s more than 200 basis points below the US federal funds rate.

In the US, neither monetary nor fiscal policy has stimulated growth. The Federal Reserve appears to be holding out for more evidence that inflation is approaching its long-term target before cutting rates, which we still expect it to do at least twice this year. On the fiscal side, we think the Trump administration’s laser-like focus on tariffs and immigration will reduce growth.

For credit investors, it’s not only tariffs that matter. It’s also the pace of tariff changes. Every new round imposed, paused or renegotiated alters the landscape and the exposures of individual companies.

None of this means that Treasuries have stopped playing a vital role in bond allocations. We strongly believe they’ll exhibit negative correlations with risk assets in cases of extreme duress while offering an attractive opportunity to increase duration exposure. But in today’s uncertain environment, a global approach seems to make sense and broadens the opportunity set.

Six Strategies for Staying on Your Toes

1. Manage duration.

Predicting the direction of bond yields over the near term is challenging. Our focus remains on the intermediate term, and we think that’s where investors should focus too. Historically, yields have declined as central banks have eased. Thus, in our view, bonds are likely to enjoy a price boost as yields trend lower in the coming two to three years in most regions.

Demand for bonds could remain exceptionally strong, in our analysis, given how much money remains on the sidelines seeking an entry point. As of June 17, $7.02 trillion was sitting in US money-market funds, a relic of the “T-bill and chill” strategy popular when central banks were aggressively hiking interest rates. Now that money-market rates are declining, we anticipate roughly $2.5 to $3 trillion will return to the bond market over the next few years.

We expect bonds, having recently resumed their traditional role as an anchor to windward, to retain that role. In other words, duration will likely be negatively correlated to equities, in our view, and we believe it should be part of an overall asset allocation.

If your portfolio’s duration, or sensitivity to changes in interest rates, has veered toward the ultrashort side, consider lengthening it. As interest rates decline, duration may benefit portfolios by delivering bigger price gains. Government bonds, the purest source of duration, also provide ample liquidity and have helped offset equity market volatility.

But don’t just set your duration and forget it. When yields are higher (and bond prices lower), lengthen your duration; when yields are lower (and prices higher), trim your sails. And remember: even if rates do rise from current levels, high starting yields provide a cushion against price declines.

2. Think global.

As monetary policies diverge, idiosyncratic opportunities increase globally, and the potential advantages provided by diversification across different interest-rate and business cycles become more powerful.

3. Focus on quality credit.

In this uncertain environment, credit has shown more resilience than stocks. Investment-grade and high-yield spreads widened when tariffs were first announced in April but have since narrowed.

When formulating an outlook for the credit markets, we believe it’s more important to focus on yield levels than on spreads. Yield has been a better predictor of return over the next three to five years than spread, even in very challenging markets. And today, yields across credit-sensitive assets are attractively high.

But current conditions demand careful security selection. Changing policies and regulations won’t affect industries and companies uniformly, nor will weaker economic growth. For instance, energy and financials are likely to face less regulation, while import-reliant industries such as retail could struggle.

We think it makes sense to underweight cyclical industries, CCC-rated corporates—which account for the bulk of defaults—and lower-rated securitized debt, as these are most vulnerable in an economic slowdown. A mix of higher-yielding sectors across the rating spectrum—including corporates, emerging-market debt and securitized assets—provides further diversification.

4. Adopt a balanced stance.

We believe that both government bonds and credit sectors have a role to play in portfolios today. Among the most effective strategies are those that pair government bonds and other interest-rate-sensitive assets with growth-oriented credit assets in a single, dynamically managed portfolio.

This pairing takes advantage of the negative correlation between government bonds and growth assets and helps mitigate tail risks such as the return of extreme inflation or an economic collapse. Combining diversifying assets in a single portfolio makes it easier to manage the interplay of rate and credit risks and to readily tilt toward duration or credit according to changing market conditions.

5. Partner up with a systematic approach.

Today’s environment also increases potential alpha from security selection. Active systematic fixed-income approaches may help investors harvest these opportunities.

Systematic strategies rely on a range of predictive factors, such as momentum, that are not efficiently captured through traditional investing. Because systematic approaches depend on different performance drivers, we believe their returns complement traditional active strategies. What’s more, these strategies are impassive: they’re not influenced by the headlines that drive investor emotion.

6. Protect against inflation.

We think investors should consider increasing their allocations to inflation strategies, given the risk of future surges in inflation, inflation’s corrosive effect and the affordability of explicit inflation protection.

Be Nimble and Be Active to Seize Opportunities

As we see it, investors should get comfortable with evolving policy expectations and near-term turbulence, while positioning portfolios to take advantage of opportunities created by periods of heightened volatility.

Above all, keep an eye on broader trends, such as slowing economic growth, attractive starting yields and pent-up demand. This is a favorable environment for bond investors, as we see it. And we believe today’s conditions may prove fruitful for bond investors poised to take advantage.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein