Income-oriented investors in Europe are no strangers to commercial real estate (CRE). With benchmark interest rates at or below zero for nearly a decade, pension funds, insurance companies and large corporations turned to investing in core property to earn income at a time when European investment-grade bonds yielded less than 1%.

This made sense: buying into a high-quality core property and financing that purchase with highly accretive debt generated high and steady income.

Since the early 2000s, core real estate equity strategies have delivered an average annualized returns about 6.7%. What made this possible? All that cheap debt, which enabled real estate investors to boost return potential.

Pivoting to Debt in a Higher-Yield Environment

Today, the base rates used as reference rates for commercial real estate loans are much higher. Put simply, leverage is no longer cheap. Instead, financing costs can exceed core property yields, making debt dilutive to investors.

With debt consuming a greater amount of a property’s cash flow, equity investors receive a lower running yield and are increasingly reliant on a property’s capital appreciation to deliver target returns, which may or may not materialize in today’s high-rate environment.

How Debt Investors May Benefit

For income-oriented investors, this creates a problem. We see a potential solution: it may be time for income-seeking investors to diversity into CRE debt. Elevated interest rates make leverage dilutive for equity investors, but they benefit investors in debt.

In the current rate environment, debt funds deliver high yields that rival or even exceed the income once generated by core CRE equity. What’s more, debt instruments carry less risk than equity funds due to their senior position in the capital structure, which governs repayment priority in the event of a default.

When considering the uncertainty in today’s market and the headwinds this can create for capital growth, we think CRE debt presents a safer alternative for investors looking to secure steady investment income.

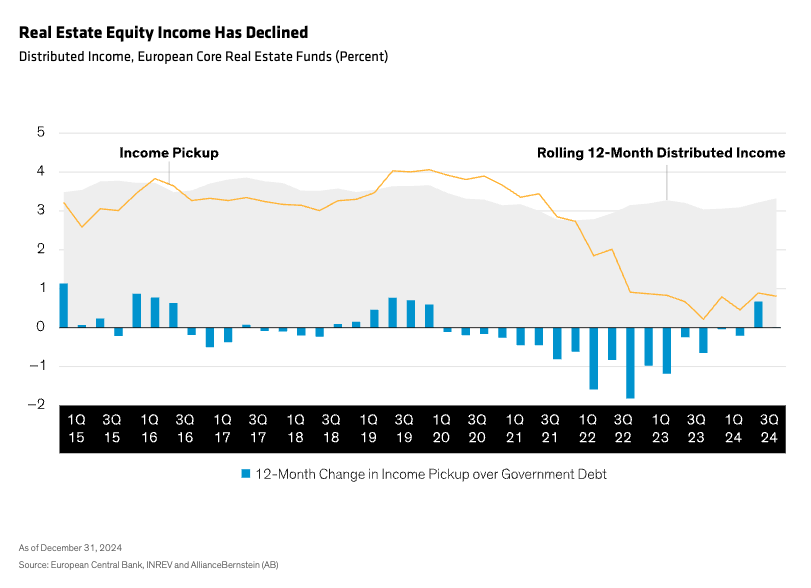

The following display shows that the income premium that European core equity funds offer over that of risk-free bonds is less than 100 basis points, a 10-year low.

Finding Order in Real Estate Income

Investors today face various risks and concerns: elevated interest rates, slower economic growth, persistent inflation, geopolitical conflict, and potential changes in the global economic landscape.

These are not ideal conditions in which to bank on capital appreciation. For income-oriented real estate investors, pivoting to debt can provide a unique opportunity to capture attractive income and benefit from greater downside protection. It may be time to get comfortable clipping coupons.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein