Nvidia’s Jensen Huang Warns China Could Overtake the U.S. in the AI Arms Race

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsNvidia CEO Jensen Huang turned heads earlier this month when he told the Financial Times he believes China will win the artificial intelligence (AI) arms race due to the country’s expanding power capacity and lack of regulatory bottlenecks that slow things down here in the U.S. Whether Huang is ultimately proven right or wrong, his comment reveals how hot the race is heating up.

No question about it, the biggest players in AI right now are the U.S. and China. Both superpowers understand that whoever leads in this still burgeoning industry will likely influence global standards, intelligence gathering, national defense, commerce and so much more for decades to come.

From where I stand, the future of AI leadership comes down to three things: chips, power and cybersecurity.

The Fight for the Fastest Silicon

The U.S. dominates when it comes to AI models. OpenAI (which launched ChatGPT three years ago this month), Anthropic, Google, Meta and others remain well ahead of the competition in terms of raw performance and global influence.

China is closing the gap faster than I think many investors realize.

Chinese firms such as DeepSeek, Alibaba and Moonshot are developing highly efficient models that deliver competitive performance while relying on fewer high-end chips. They’re also pushing hard into open source software (OSS), which is expected to accelerate adoption rates across the globe.

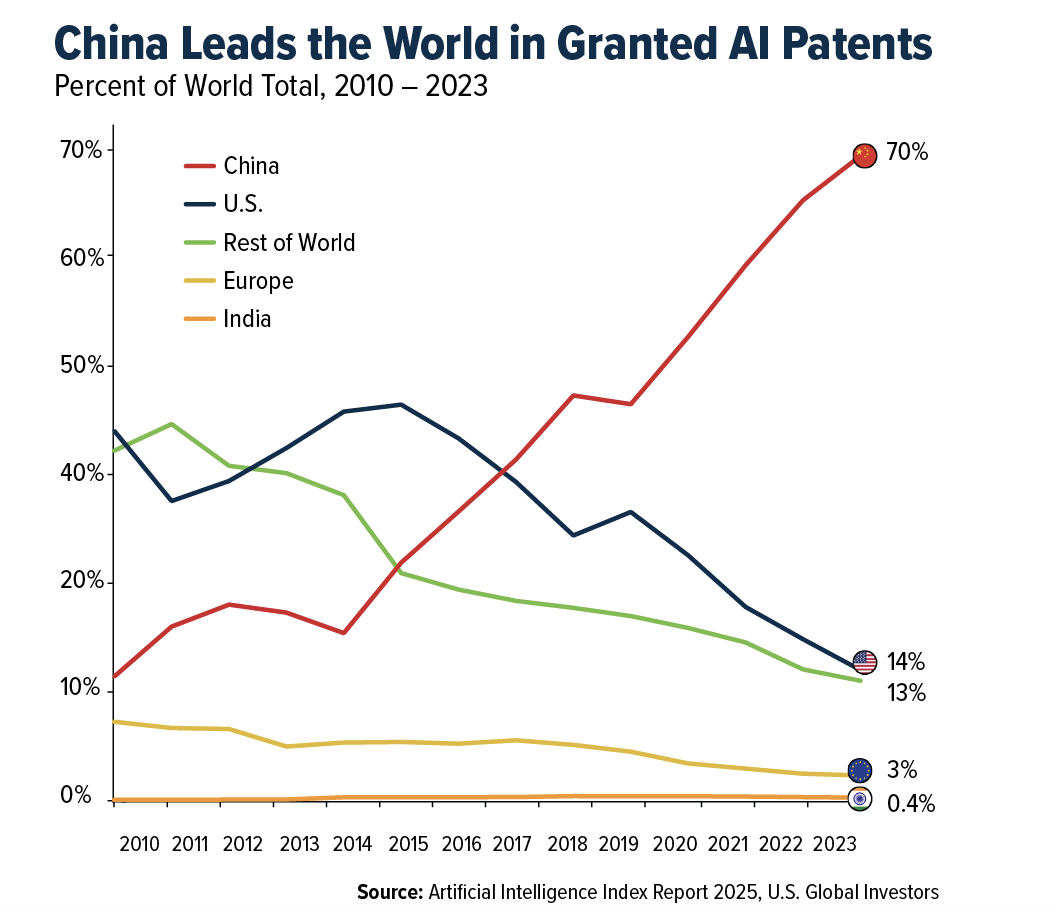

The patent landscape shows just how serious Beijing is. Roughly 70% of all AI-related patents now originate from China, according to Stanford University’s 2025 AI Index Report. Compare this to the U.S., which accounts for around 14%, a figure that’s been declining overall since 2010.

Not every patent translates into commercial success, of course, but they’re an early indicator of national priorities. China wants to be the global hub for AI research and development, and it’s using every tool available to get there.

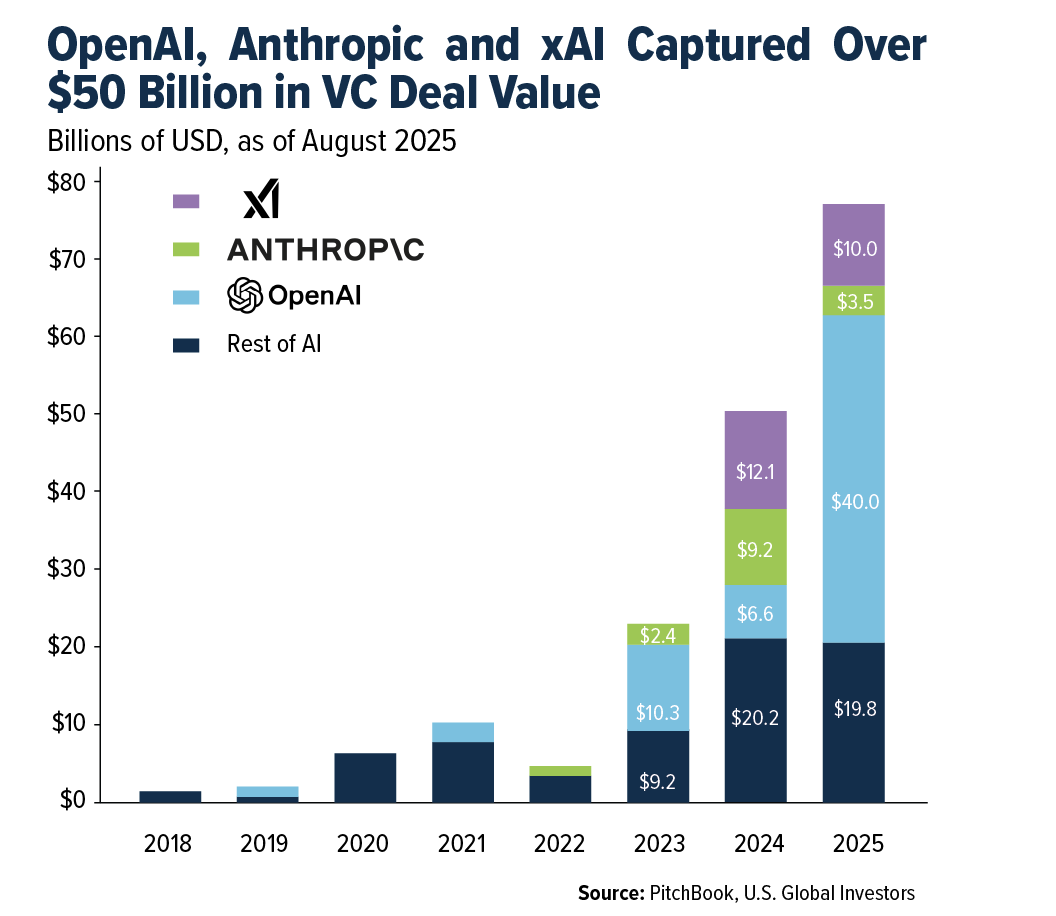

Meanwhile, U.S. venture capital has become increasingly concentrated. More than 40% of all AI deal value has gone to the top 10 companies raising money this year, with only three companies—OpenAI, Anthropic and xAI—capturing over $50 billion combined through the end of August, according to PitchBook. That’s a lot of capital flowing to a very small group of players.

At U.S. Global Investors, we hold positions in several companies involved in AI chips and cybersecurity platforms, and we continue to see strong momentum in the deployment of compute power. But make no mistake, the competition is intensifying.

The Kilowatt Arms Race

As we all know, training large-language models (LLMs) consumes enormous amounts of electricity, and data centers are popping up faster than many utilities can keep up.

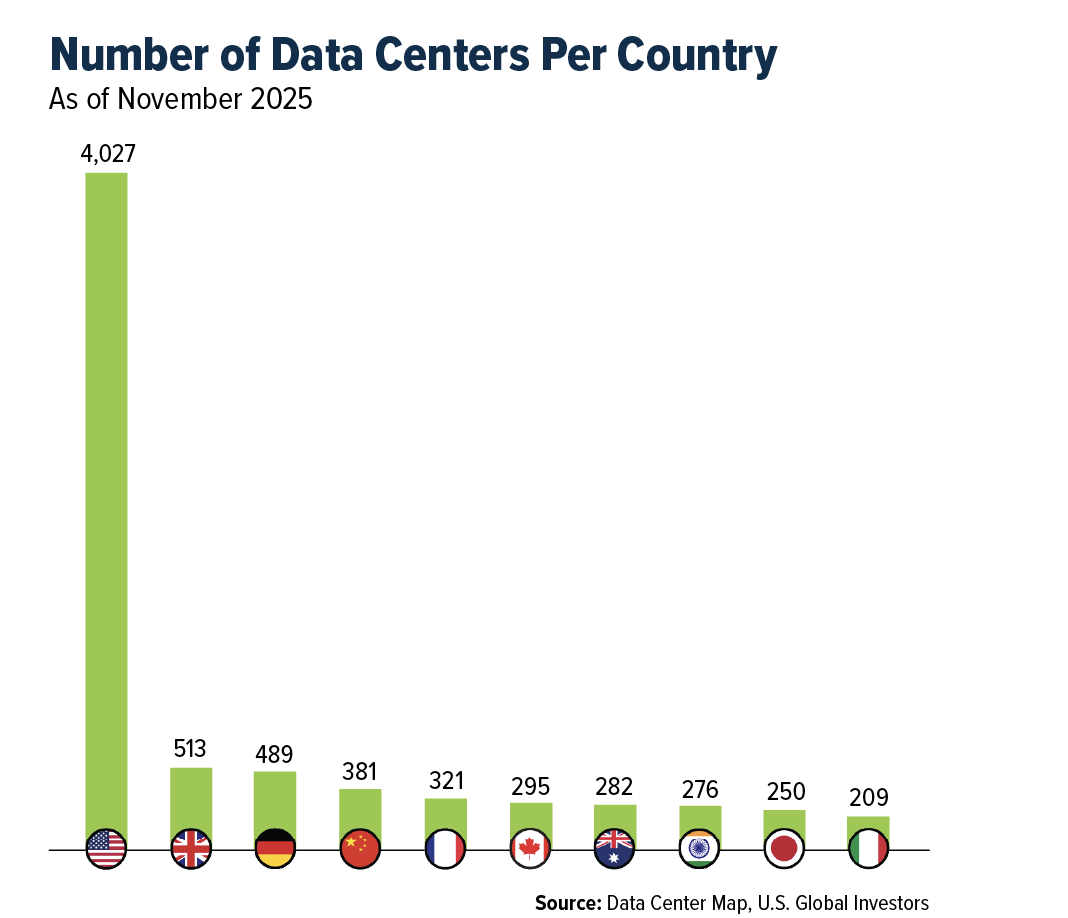

The U.S. hosts nearly half the world’s data centers—more than 4,000 currently, compared to the U.K. in the number two slot with just over 500 data centers—but as is the case with AI models, China is catching up.

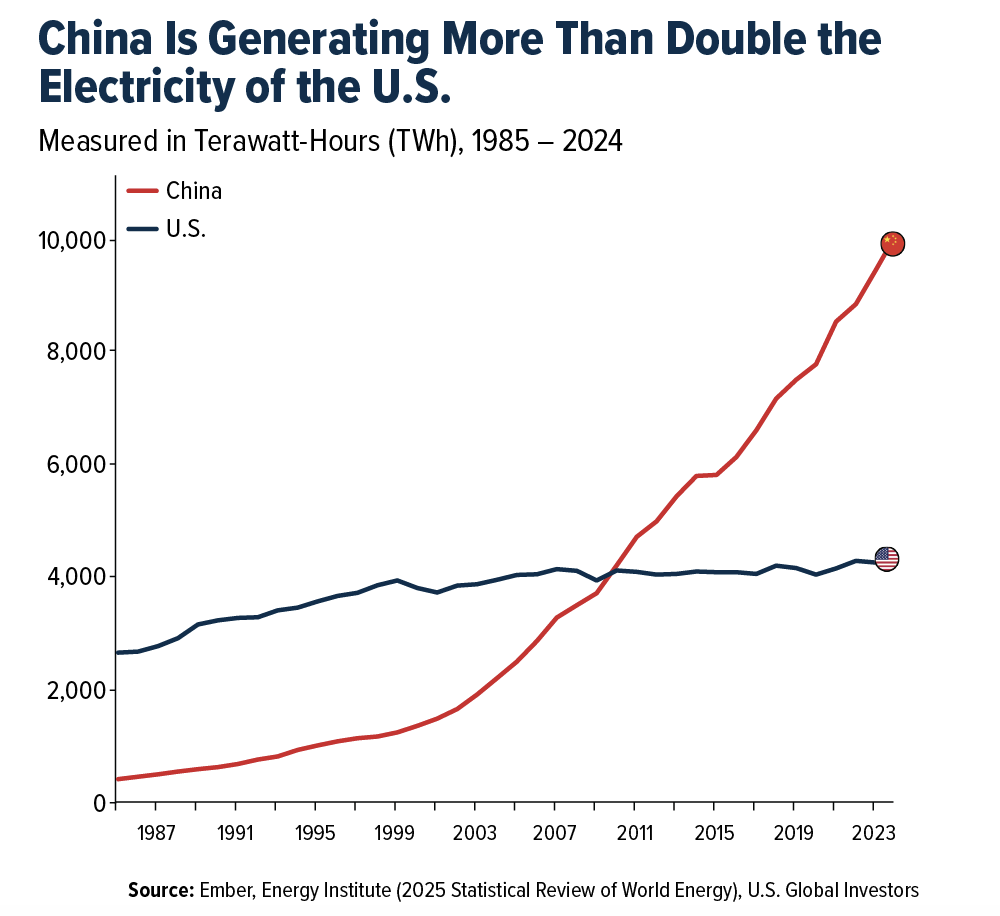

Another area where China is surpassing the U.S.? Energy. In an open letter to Michael Kratsios, executive director of the Office of Science and Technology Policy, OpenAI warned that the U.S. is falling behind China, threatening America’s edge on AI, “the most consequential technology since electricity itself.” The tech firm pointed out that China added an astounding 429 gigawatts (GW) of brand new power capacity in 2024, while the U.S. added only 51 GW.

I’m not suggesting that China is guaranteed to win. The U.S. still leads in high-value chips, large-scale model development and private-sector innovation. But power availability and cost are becoming the decisive factors in AI expansion. Nvidia’s Huang has said many times that electricity will determine who can scale AI, and the data is starting to support that view.

Cybersecurity: The New Front Line

The third front in the U.S.-China AI rivalry is digital security. The past year has seen one of the most dramatic escalations in cyber risk that the world has ever seen.

Anthropic, the AI platform that hosts the Claude chatbot, recently revealed the first documented case of a China-linked group using an AI agent to run an entire espionage campaign. The AI handled everything, from reconnaissance to data extraction. Human operators, which Anthropic noted were probably not very sophisticated coders, acted more like supervisors than attackers. Nearly 30 targets were attacked, with AI completing most of the work all on its own.

Meanwhile, U.S. cybersecurity firms are building defensive AI agents that can respond to threats in real time. Palo Alto Networks, which we held in our defense tech ETF as of September 30, has been integrating generative-AI capabilities across its platform and rolling out agent-based tools. The company has also been expanding through acquisitions, announcing this week that it bought cloud-native observability platform Chronosphere for $3.35 billion.

There’s real urgency here. This year, the average cost of a data breach in the U.S. hit $10.2 million, a new record high and the highest cost anywhere in the world, according to IBM.

Final Thoughts

I believe the U.S.-China tech rivalry will guide the direction of AI for years to come. Both nations are moving quickly, and the technologies involved are advancing at a pace we really haven’t seen since at least the early days of the internet. That’s why we hold long-term positions in several firms across the themes I discussed.

As always, stay curious and stay informed!

If you’d like to learn more about investment opportunities in AI and cybersecurity, send an email to [email protected] with the subject line CYBER.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Bombardier, up 1.4%. LATAM Airlines reported a beat from top to bottom line in third quarter 2025 results, surpassing JP Morgan estimates. The company delivered U.S.$1,150 million in ad

- Air cargo volumes for October grew 4% year-over-year (YoY) boosted by strong Asia Pacific volumes (+10% YoY) boosted by Taiwan and ASEAN tech-related flows, according to Bank of America.

- The Federal Aviation Administration (FAA) ended mandated flight cuts following a decline in staffing concerns. On Monday morning, the FAA fully lifted this order, noting that there has been a steady decline of staffing trigger events at ATC facilities.

Weaknesses

- The worst-performing airline stock for the week was Amadeus, down 8.5%. China’s Foreign Ministry, along with Chinese embassies and consulates in Japan, advised Chinese citizens to avoid traveling to Japan. According to Goldman, if inbound demand from China in 2026 decreases by 20% year-over-year (YoY), Japan’s total inbound demand for 2026 would still be up 2% year-over-year. Chinese visitors were the top inbound group in September 2025, up 19% year-over-year (YoY) and accounting for 23% of Japan’s foreign inbound travelers.

- Global air cargo rates are averaging 9% lower year-over-year (YoY) for the fourth quarter of 2025 so far. The data shows that YoY rate declines appeared to ease in the second half of October, helped by front-loading ahead of tariff threats, according to Bank of America.

- LATAM Airlines canceled 173 flights amid a pilot strike. The airline canceled at least 173 flights and affected 20,000 passengers after pilots went on strike following failed union negotiations, according to JP Morgan.

Opportunities

- Grupo Sureste (ASUR) and Motiva announced that the companies have entered into an agreement for the sale of Motiva’s airports segment to ASUR. The assets to be sold were valued at an equity value of 5 billion Brazilian reais (BRL) for an implied enterprise value of 11.5 billion Brazilian reais (BRL). A successful sale is expected to significantly reduce leverage (from 3.5 times currently to below 3.0 times post-deal) while also allowing the company to reduce net debt at the holding level and de-risk the portfolio.

- Cargo supply has grown an average of 3% year-over-year (YoY) over the past four weeks. Bank of America notes that capacity continues to be withdrawn from North America (down 2% YoY) and redeployed to Europe (up 4% YoY) due to shifting supply chains. There may be potential supply disruption from the recent U.S. regulator decision to ground all MD-11 aircraft, which represent 9% and 5% of UPS and FedEx fleets, respectively.

- The biannual Dubai Airshow was hosted in the United Arab Emirates, with Airbus and Boeing both receiving large aircraft orders. Boeing led Day 1 of the show with a total of 85 aircraft orders. Airbus, however, delivered a much stronger performance on Day 2, receiving 212 orders, according to RBC.

Threats

- Comments from IAG CEO Luis Gallego included his remark that corporate traffic volumes at British Airways are below 70% of 2019 levels, while revenues are at about 85% of 2019 levels. In comparison, corporate volumes at Iberia and Aer Lingus—also owned by IAG—are close to 100% for both.

- According to Goldman, Yangzijiang Shipbuilding held an analyst briefing following its third-quarter 2025 business update. The company is cautious on its guidance, citing weaker demand for containerships and increased competition from tier-two shipyards. Management noted: (1) a potential decline in new containership orders and a 10% drop in new-build prices in 2026, given worsening profitability for container lines and lower pricing from tier-two shipyards.

- According to Morgan Stanley, the U.S. Administration plans to withdraw a proposed compensation rule that would require airlines to compensate passengers for significantly delayed or canceled flights. They may also roll back President Biden’s regulations requiring airlines and ticket agents to disclose service fees alongside airfares.

Luxury Goods and International Markets

Strengths

- LVMH is ramping up its China expansion after its ship-themed pop-up in Shanghai became a surprise hit, suggesting the country’s multiyear luxury slump may finally be bottoming out. Analysts caution the rebound will be slow, as Chinese consumers are still weighed down by the housing crash, weak job prospects, and low confidence, meaning brands must work harder to excite shoppers with fresh designers, new store experiences, and culturally relevant collaborations.

- Porsche has unveiled the first electric Cayenne, delivering up to 1,139 horsepower and reaching 0–100 kilometers per hour in 2.5 seconds. The model is the most powerful car in the brand’s history and the world’s first mass-produced vehicle to support wireless charging. Inside, it features a massive curved display, and the range is rated at nearly 650 kilometers. Sales will begin in summer 2026 with a starting price of $111,000, or 9 million rubles.

- Star Entertainment Group, an Australian hotel, casino owner and operator, was the best-performing S&P Global Luxury stock, rising 20.47% over the past five days after regulators in Queensland and New South Wales approved Bally’s and Investment Holdings’ plan to convert A$300 million of debt into equity, paving the way for new board appointments and a change of control at the embattled casino operator.

Weaknesses

- An 18-year-old girl on a Carnival cruise was found dead in her cabin wrapped in a blanket and life jackets and hidden under a bed, reports Yahoo, after she left dinner feeling sick. Now the FBI is investigating this case on the luxury cruiseliner since it happened in international waters.

- Tesla is recalling over 10,000 Powerwall 2 batteries nationwide, reports CNBC, after multiple overheating, smoke, and fire incidents caused by a defective third-party cell. The company is now remotely disabling affected units and replacing them for free.

- Shiseido Co. Ltd., the cosmetics manufacturer, was the worst-performing S&P Global Luxury stock, falling 18.43% over the past five days after Beijing warned its citizens against traveling to or studying in Japan, raising concerns about a sharp drop in Chinese tourist spending—a key revenue driver for Japan’s retailers and cosmetics brands such as Shiseido.

Opportunities

- Automakers plan to invest about 25 billion dollars in hybrid and electric vehicle production in Brazil by 2030, led by Stellantis and Volkswagen, as rising import taxes and pro-industry policies drive the market toward electrification. Electrified vehicle sales are surging, but challenges remain, including limited fast-charging infrastructure and long-distance range concerns, even as buses, trucks, and light commercial fleets adopt electric and hybrid technologies more quickly.

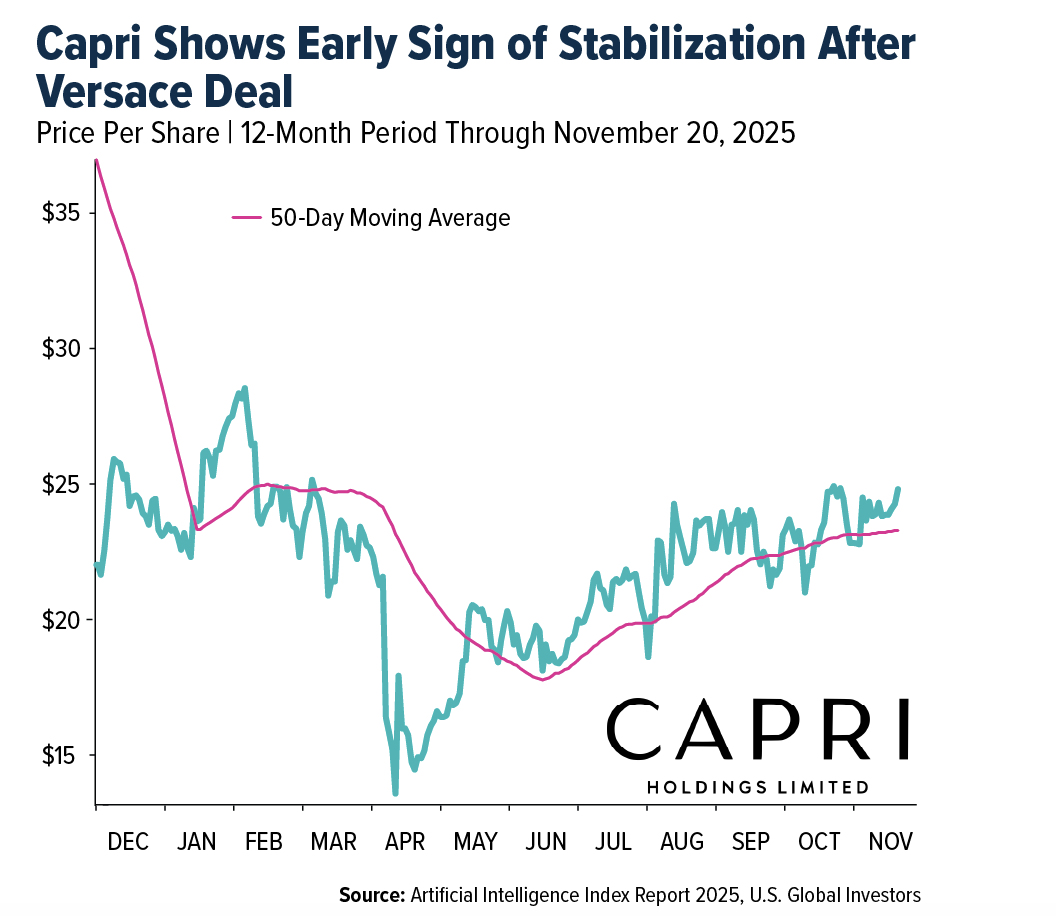

- Capri is resetting as it sells Versace to Prada for about $1.38 billion, using the proceeds to reduce roughly $1.5 billion in net debt and fund a $1 billion share buyback from fiscal year 2027, while refocusing on Michael Kors and Jimmy Choo through new designs, store upgrades, and data-driven client acquisition. Despite macro headwinds, high U.S. exposure, and tariff risk, management targets flat-to-modest growth in fiscal year 2026 with adjusted earnings per share of $1.20 to $1.40, laying the groundwork for a return to revenue and profit growth in fiscal year 2027.

- Prada’s Lorenzo Bertelli said the group may consider more acquisitions after buying Versace, and he didn’t rule out future interest in Armani, even though he stressed there have been no discussions at all. He’s preparing to take on a bigger role, including becoming executive chairman of Versace and eventually CEO of Prada, as the family focuses on turning Versace around and shaping the company’s long-term succession strategy.

Threats

- France’s state auditor criticized the Dutreil inheritance tax break as overly generous, costing the government more than 5.5 billion euros last year without boosting investment or preventing family companies from being sold. The report calls for tougher rules, including longer holding periods, stricter asset eligibility, and smaller tax benefits, while the government signals it wants to keep the regime but narrow it amid political pressure to tax the rich.

- Kering shares fell after reports that CEO Luca de Meo told staff the company must reduce its reliance on Gucci, rethink years of aggressive price hikes, and scale back its store network as part of an 18-month turnaround plan. De Meo aims to revive growth across all brands, including Saint Laurent, Bottega Veneta, and Balenciaga, with a full strategic reset for investors next spring, though analysts note the memo offers few concrete details and a return to Gucci’s former momentum remains distant.

- JD Sports warned full-year profits will land at the lower end of expectations as rising unemployment, weak consumer sentiment, and an unusually warm autumn weigh on demand. The retailer reported ongoing sales declines across the UK, Europe, and North America, although trends improved slightly from the prior quarter, while Asia Pacific was the only region to post growth.

Energy and Natural Resources

Strengths

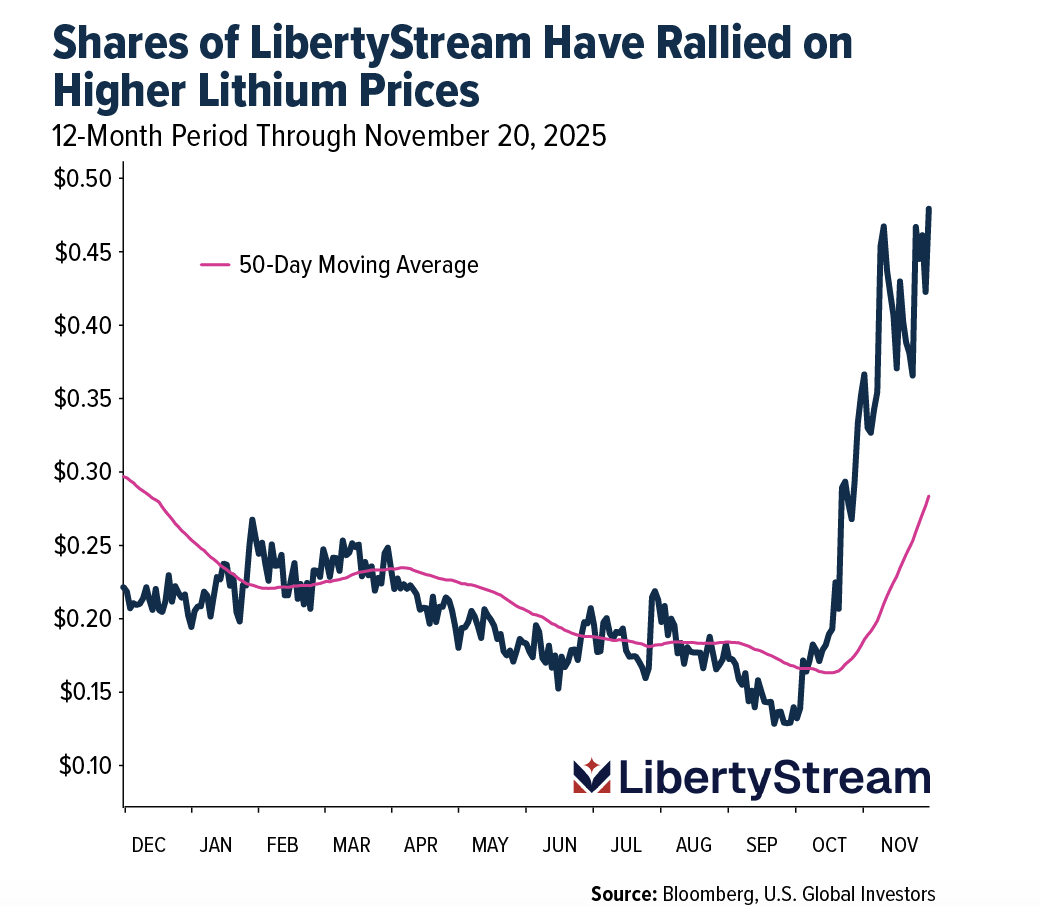

- The best-performing commodity for the week was lithium, up 5.73%. Mineral Resources’ lithium asset sale to POSCO was viewed positively by Fitch, strengthening the company’s balance sheet by reducing leverage and stabilizing its outlook. The transaction underscores ongoing confidence in lithium valuations and reinforces the sector’s resilience as strategic buyers continue acquiring high-quality spodumene assets. LibertyStream stands out as a company positioned to benefit as lithium emerges from a supply glut.

- TotalEnergies’ acquisition of 50% of European power assets strengthens its transition into low-carbon electricity, expanding generation and retail scale across key EU markets. The move keeps the company on track to achieve 20% of total energy sales from electricity by 2030, reinforcing its leadership in the fast-growing power sector.

- Algoma Steel’s completion of a $500 million government-backed financing package significantly strengthens its balance sheet and provides long-term liquidity to support its transition to lower-carbon Electric Arc Furnace technology. The financing enhances operational flexibility, reinforces government–industry alignment, and positions Algoma as a more competitive, modern, and sustainable North American steel producer.

Weaknesses

- The worst-performing commodity for the week was lumber, down 10.25%. Prices softened as winter approached, with demand weak despite recent curtailments and ample inventories. Traders and sawmills faced intensified competition for limited orders, reflecting ongoing softness in construction and housing activity.

- China broadened its restrictions on BHP, ordering steel mills and traders to halt purchases of additional products such as Jingbao/Jinbao fines, extending earlier bans tied to stalled contract negotiations. The move increases pressure on BHP by closing blending workarounds, requiring CMRG approval for dollar-denominated or port-sourced cargoes, and further limiting access to the world’s largest iron ore buyer.

- Freeport-McMoRan’s upcoming Grasberg recovery update is expected to align with prior guidance, given the company’s strong operational track record, though ongoing government review poses a risk of delays. Copper and gold sales are projected to remain below pre-incident levels through 2026, with adjusted free cash flow expected to drop 52% to $1 billion in 2025, followed by further declines in both copper and gold volumes next year.

Opportunities

- The U.S. is providing a $1 billion federal loan to restart Three Mile Island’s Unit 1 reactor, enabling Constellation to bring the once-mothballed plant back online by 2027 under a long-term power agreement with Microsoft, which will supply carbon-free electricity for its data centers. The move marks a symbolic reversal for a site long associated with nuclear risk, reflecting a broader shift in U.S. energy policy as tech companies turn to nuclear to meet AI-driven power demand.

- Cochilco raised its copper price forecasts to record highs, now expecting $4.45 per pound in 2025 and $4.55 per pound in 2026, citing weak Chilean production and persistent supply constraints. The commission warned of ongoing risks, such as tariffs and shifting demand trends, but still sees copper on an upward trajectory through 2030 as supply struggles to keep pace.

- China is considering a nationwide property-stimulus package, including mortgage subsidies for first-time buyers, higher tax rebates, and lower transaction costs, to stabilize its weakening housing market and prevent broader financial strain. If implemented, these measures could reignite construction activity, which would be bullish for industrial metals and copper, given their heavy use in housing, electrical wiring, appliances, and infrastructure tied to real-estate development.

Threats

- China’s latest $8.6 billion dual-currency bond issuance drew a record $234 billion in bids, allowing Beijing to borrow in dollars at nearly the same cost as the U.S., despite its lower credit rating. The surge in global demand signals a major shift in capital from heavily indebted developed markets toward Chinese sovereign debt.

- The volume of oil on water has surged to nearly 1.4 billion barrels, an all-time high, creating a significant threat to market stability. This glut of unsold crude increases the risk of price volatility, storage congestion, and forced discounting as barrels compete for a final destination.

- A deepening global LNG oversupply poses a threat to natural gas producers and exporters, as Asian and European prices are expected to fall and erode margins. Prolonged weakness also pressures import-dependent markets by discouraging long-term contracting and weakening investment signals across the supply chain.

Bitcoin and Digital Assets

Strengths

- SoftBank’s PayPay is expanding crypto access in Japan. PayPay, one of the world’s largest consumer payment networks, has integrated with Binance Japan, enabling instant, low-cost crypto deposits and withdrawals. Adoption by a major Japanese financial institution boosts legitimacy, lowers barriers to buying Bitcoin, and broadens access to millions of retail users ahead of PayPay’s expected U.S. IPO.

- Coinbase is expanding strategic leadership in on-chain trading. Its acquisition of Vector, a Solana-native decentralized-exchange platform, strengthens Coinbase’s role as a leading on-chain trading hub and accelerates support for Solana’s rapidly growing ecosystem, which surpassed 1 trillion U.S. dollars in cumulative decentralized-exchange volume this year. Integrating Vector’s technology will improve order routing, token access, and execution quality as Coinbase advances its “everything exchange” strategy across Bitcoin, Solana, and the wider digital-asset market.

- According to CoinMarketCap, among the top 100 crypto coins and tokens, the top gainers over the past seven days were Starknet (STRK), up 25%; MYX Finance (MYX), up 12%; and Aster (ASTER), up 11%.

Weaknesses

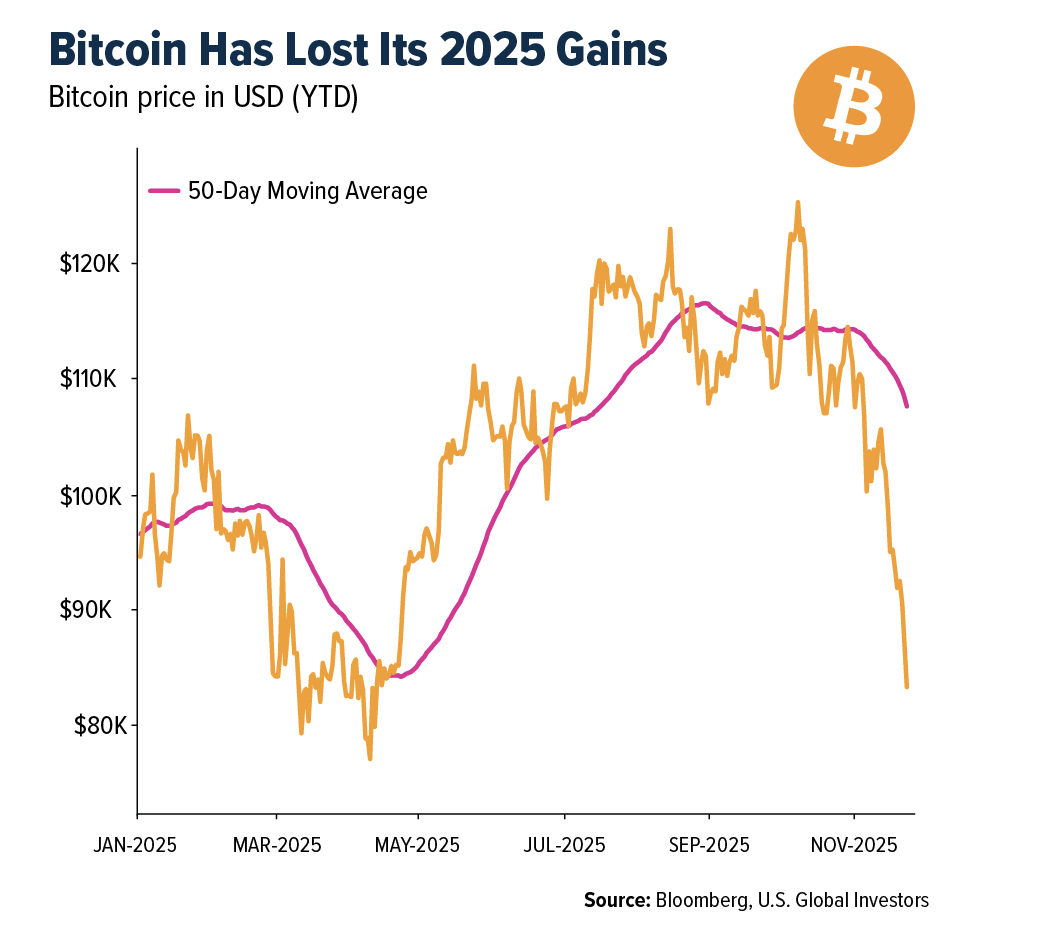

- Bitcoin is failing to rally despite strong tailwinds. Bitcoin’s sharp retreat from its 126,000-dollar peak—now trading near 83,000 dollars and down 10.44% year-to-date—signals weak conviction despite Wall Street support, political momentum, and institutional inflows. It marks Bitcoin’s worst monthly decline since the 2022 crypto winter, wiping out all 2025 gains. The loss of 600 billion dollars in Bitcoin’s market value and more than 1 trillion dollars across the broader crypto market, paired with fading retail participation and fragile liquidity, highlights structural vulnerabilities and renewed fear of another halving-cycle downturn.

- A U.S. national security probe is putting Bitcoin mining supply chain at risk. The U.S. is investigating Bitmain—producer of more than 80% of global Bitcoin ASICs—over potential national security concerns, including alleged remote-control capabilities that could compromise critical infrastructure. With Bitmain and MicroBT controlling 97% of the ASIC market, any restrictions or seizures could threaten the entire U.S. mining sector. Past shipment halts and rising geopolitical tensions underscore how heavily Bitcoin’s infrastructure relies on foreign hardware, exposing miners to significant supply-chain and regulatory risks.

- According to CoinMarketCap, among the top 100 crypto coins and tokens, the largest decliners over the past seven days were Morpho (MORPHO), down 26.36%; Canton (CC), down 26.32%; and Story (IP), down 25.63%.

Opportunities

- Institutional dip-buying has signaled renewed confidence in digital assets. Ark Invest’s back-to-back purchases—nearly $40 million per day across Coinbase, Circle, Bullish, and Bitmine—highlight growing institutional conviction during a market sell-off. While the CoinDesk 20 Index fell 4.7%, Ark increased exposure, treating lower valuations as an entry point rather than a warning sign.

- Japan’s $135 billion stimulus injects liquidity that can support digital assets. The package adds significant liquidity to the global economy, creating a favorable environment for risk assets. Greater liquidity often boosts demand for alternatives like Bitcoin, and easing financial conditions in major economies may drive renewed inflows and improved crypto market sentiment.

- Stronger institutional infrastructure can boost Bitcoin adoption. GSR, a leading crypto liquidity provider, upgraded GSR One to offer more transparent, reliable trading with institutional-grade market making, over-the-counter trading, and treasury services. By aligning crypto execution and liquidity with traditional finance standards, the market becomes safer and more efficient, increasing institutional confidence and supporting broader Bitcoin adoption.

Threats

- Brazil’s new FX rules are tightening stablecoin control. Brazil, Latin America’s largest economy, will tax stablecoin-based international payments by classifying all stablecoin activity as foreign-exchange transactions starting in February. With R$227 billion ($42.8 billion) in crypto volume in H1 2025, two-thirds in USDT, the rules aim to curb regulatory arbitrage and could sharply raise costs for users and firms. Authorities estimate over $30 billion in annual revenue lost to crypto-based imports, signaling stricter enforcement ahead and potential strain on stablecoin use and cross-border flows.

- Record ETF outflows have revealed fading retail confidence. Spot Bitcoin and Ethereum ETFs saw $3.79 billion in outflows in November, with BlackRock’s IBIT alone losing over $2 billion. JPMorgan analysts attribute the sell-off mainly to retail investors, contrasting with $96 billion retail inflows into equity ETFs over the same period. The divergence highlights weakening conviction in digital assets and a shift toward safer traditional investments.

- MSCI may exclude crypto treasuries, triggering forced selling. MSCI is considering removing companies with over 50% of assets in Bitcoin or other crypto, a move analysts call “highly likely.” This would force index-tracking funds to sell affected stocks, potentially wiping out $2.8 billion in strategy-specific holdings and impacting $9 billion in passive index vehicles. With 38 companies—including major miners and treasuries—on MSCI’s radar, the change signals a more conservative approach from index providers and rising reclassification risk across equity benchmarks.

Defense and Cybersecurity

Strengths

- NVIDIA delivered a dominant quarter, with revenue up 16 percent year-over-year, datacenter revenue up 27 percent year-over-year, and NGS annual recurring revenue growing 29 percent year-over-year to 5.85 billion dollars. Gross margin held near record levels at 75 percent non-GAAP, driven by Blackwell Ultra, which now accounts for roughly two-thirds of Blackwell revenue. The results highlight strong visibility toward a 500 billion dollar-plus datacenter cycle by 2026, supported by hyperscale demand, sovereign AI initiatives, and enterprise AI adoption.

- Microsoft, NVIDIA, and Anthropic have formed a major strategic AI alliance under a $45 billion framework, with Microsoft investing over 5 billion dollars, NVIDIA committing up to 10 billion dollars, and Anthropic agreeing to spend about 30 billion dollars on Azure, deepening demand for NVIDIA’s AI infrastructure stack.

- MOOG Inc. was the best-performing stock in the XAR ETF this week, rising 6.63% after reporting record fourth quarter sales of about $1.05B (+14% YoY) and guiding FY26 revenue to $4.2B and adjusted EPS to $10.00, both above consensus (≈$4.0B and ≈$9.6). The company also signaled further margin expansion and stronger free cash flow.

Weaknesses

- Cloudflare experienced a significant outage on November 18 due to a hidden bug in its bot protection system, causing widespread internet disruptions. A Japanese court also ordered Cloudflare to pay damages for inadequate identity verification procedures, marking a notable precedent in copyright enforcement.

- European defense stocks slumped and oil names fell while airlines and chemicals rallied after Zelenskiy agreed to review a U.S.-Russia draft peace plan that would require major concessions from Ukraine, triggering broad sector moves tied to ceasefire expectations.

- Rocket Lab Corp. was the weakest stock in the XAR ETF this week, falling 11.51% after a director disclosed a $2.72 million open-market sale of 60,400 shares, adding to negative sentiment around the stock despite its recent launch successes.

Opportunities

- The U.S. Department of Energy approved a $1 billion loan to restart the Three Mile Island nuclear reactor, which is expected to supply power to Microsoft data centers under a 20-year agreement, supporting long-term cloud and AI capacity needs.

- IBM has expanded its Storage Scale System 6000 line, tripling maximum capacity to 47 petabytes per rack to better support AI training and other data-intensive workloads.

- Northrop Grumman’s Pegasus XL rocket has been selected for a NASA-funded mission led by Katalyst Space Technologies to raise the orbit of NASA’s Neil Gehrels Swift Observatory under a $30 million contract, with launch planned by mid-2026 to prevent reentry by the end of the year.

Threats

- Anthropic revealed the first confirmed case of fully AI-orchestrated cyber espionage, where a Chinese state-sponsored group automated 80 to 90 percent of its attack workflow, including recon, exploit validation, credential harvesting, lateral movement, and data collection. This reduces the effectiveness of traditional detection but makes deception technologies more powerful, as autonomous AI agents inevitably interact with decoys, generating early, high-fidelity signals of intrusion.

- A massive ransomware wave hit U.S. municipalities on November 20, 2025, with Attleboro, Massachusetts, forced to shut down phones, email, and core services. The attack highlights an accelerating national crisis, as sophisticated ransomware gangs like Qilin systematically target local governments, exploiting outdated systems and limited cybersecurity budgets.

- CISA ordered U.S. federal agencies to urgently patch a newly discovered and actively exploited Fortinet FortiWeb zero-day (CVE-2025-58034), a root-level OS command-injection flaw linked to ongoing attacks alongside a second FortiWeb zero-day, underscoring Fortinet’s growing role as a high-risk entry point in cyber-espionage and ransomware campaigns.

Gold Market

This week gold futures closed the week at $4,054.7, down $39.50 per ounce, or 0.96%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.35%. The S&P/TSX Venture Index came in off 2.85%. The U.S. Trade-Weighted Dollar rose 0.86%.

Strengths

- The best-performing precious metal for the week was gold, still down 0.96%. Gold is set for a small weekly decline as rate-cut expectations fade, though geopolitical tensions, after Ukraine and European allies rejected key parts of a U.S.-Russian peace framework, helped bullion trim losses. Despite short-term pressure from stronger jobs data and higher rate expectations, gold remains supported by haven demand amid global uncertainty and is on track for one of its strongest annual performances since 1979.

- Tether’s aggressive expansion into bullion is drawing gold closer to the speculative orbit that drives crypto price swings. The stablecoin issuer has been purchasing more than a ton of bullion a week and signaled its ambition by hiring HSBC’s top metals traders, according to Bloomberg.

- China added an estimated 15 tons of gold to its foreign exchange reserves in September as central banks accelerated bullion purchases after a seasonal summer lull, according to Goldman Sachs. Analysts estimate central bank purchases totaled 64 tons for September, more than tripling the 21 tons in August. Purchases likely continued in November, said Goldman.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 2.85%. The LME’s decision to stop administering the benchmark platinum and palladium auctions threatens price discovery by disrupting a long-established, highly liquid mechanism used to settle contracts across the industry. Transitioning to a new, yet-to-be-named venue introduces uncertainty, potentially reducing transparency and widening spreads in already thinly traded palladium markets.

- According to CIBC, Barrick Gold expects annual gold production to come in at the lower half of its maintained guidance of 3.15–3.50 million ounces. The company noted on a conference call that it expects production guidance for 2026 could come in relatively flat year-over-year.

- According to Goldman, gold production moderated in the current quarter due to planned seasonal maintenance, lifting sector average unit all-in sustaining costs on higher sustaining capital expenditures and nominal AISC. However, they still see eased cost pressures and rising production moderating overall unit cost increases, with persistent cost inflation at 3–5%.

Opportunities

- According to Scotia, the streamers and royalty companies have been very active this year on the transaction front, with deals totaling 9 billion dollars year-to-date. The focus remains on precious metals, with opportunities in both development-stage and producing assets, mainly for asset purchases and mine builds. Wheaton and Franco-Nevada are best positioned for larger deals, with total liquidity of over 2 billion dollars.

- Elliott Management has taken a major stake in Barrick Mining after the gold producer failed to fully benefit from a strong gold price rally, according to The Financial Times’ Leslie Hook, Oliver Barnes, and Arash Massoudi. The investment, now among Barrick’s ten largest, has fueled speculation about potential asset sales or a break-up as the company refocuses on its North American operations following its CEO’s abrupt departure.

- According to Scotia, Equinox Gold announced it has achieved commercial production at its 100 percent-owned Valentine gold mine in Newfoundland and Labrador. Valentine is now expected to deliver at the higher end of the fourth quarter 2025 production range of 15–30 thousand ounces of gold and reach nameplate capacity by the second quarter 2026, resulting in 150–200 thousand ounces of gold produced in 2026.

Threats

- Indonesia plans to start charging duties on gold exports as soon as this month to capitalize on the precious metal’s price rally this year and encourage domestic processing. Levies ranging from 7.5 percent to 15 percent will be imposed, with less processed variants subject to higher rates, according to senior Finance Ministry official Febrio Kacaribu.

- According to CIBC, B2 Gold reduced annual production guidance at Goose to 50–80 thousand ounces, down from 80–110 thousand ounces previously, due to crushing plant issues and lower-than-budgeted gold grades. Management noted the delay was caused by a lack of equipment parts and operators, which has now been resolved.

- According to JP Morgan, upside tariff risk is most acute in palladium, but longer-term prices are expected to decline as demand structurally rolls over. In the near term, heightened tariff risk will likely continue to support palladium prices. However, once flows adjust with greater tariff clarity, they expect this support to fade as the market moves back toward balance by 2027.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2025):

LATAM Airlines

Grupo Aeroportuario del Surest

Boeing

Airbus

LibertyStream Infrastructure

Total Energies SE

BHP Group

Freeport-McMoRan

Barrick Gold

Franco-Nevada

LVMH Moet Hennessy

PRADA SpA

Tesla Inc.

Carnival Corp.

Kering SA

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All