Key Takeaways

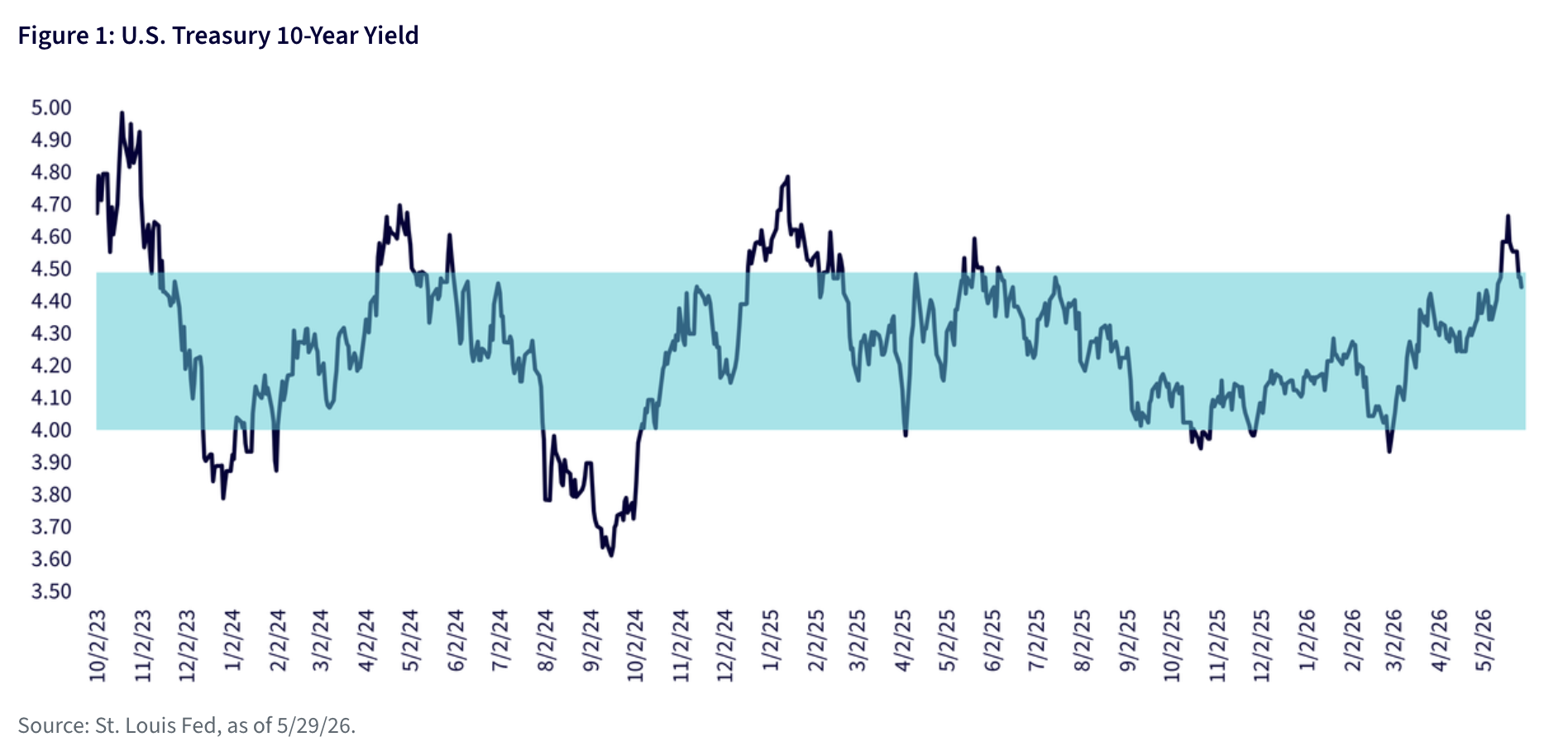

- With the 10-year Treasury yield pulling back from 4.67% but still within its 4.0%–4.5% range, employment and inflation data remain the main drivers of bond market direction.

- Despite speculation that Bessent could shift issuance toward shorter maturities, large deficits and Treasury’s commitment to “regular and predictable” issuance make that unlikely.

- With supply pressures potentially returning in 2027, investors should consider a barbell approach to their fixed income portfolio.

The rise in U.S. Treasury (UST) yields, specifically the ten-year note, since late February has captured the attention of global investors in a very visible fashion. Just a couple of weeks ago, headlines were blaring that the UST 10-year yield had reached its highest level since the beginning of 2025, leaving market participants to wonder: What comes next?

‘What comes next?’ is actually a two-part question. The first aspect is determining whether the yield will rise further or has reached another peak and will begin to decline. Traditional and social media have been abuzz about the second aspect of the question, which centers on conjecture that the Trump Administration could implement a strategy to arrest further increases in—or ‘cap’—the 10-year yield.

However, before we address this part of the question, it’s important to look at the recent path of the UST 10-year yield and the reasons behind the movement.

Recent Perspective

The 10-year Treasury yield has largely remained range-bound between 4.0% and 4.5% over the past three years, and we expect that trend to continue. While yields may overshoot or undershoot in the short term, they have consistently reverted to this range as markets react to changes in employment and inflation, the Treasury market’s primary drivers. Technical analysis currently still supports this range.

Notably, the sharpest yield spikes have come when strong economic data coincided with concerns about Treasury supply. First, in October 2023, the 10-year peaked at 4.99%. This was due to continued inflation pressures, a solid labor market and increased Treasury auction sizes. A similar dynamic occurred in January 2025, when the 10-year peaked at 4.79%. There was solid payroll growth, along with expectations that fiscal policy could increase the budget deficit and, therefore, Treasury supply.

More recently, the 10-year Treasury yield has fallen from its latest peak of 4.67% as headlines regarding a Middle East peace deal have taken center stage. The primary focus has been on developments in the Middle East and inflation. As in the 2023 and 2025 episodes, investors could face increased auction sizes in 2027.

Read more: Falling Yields Reinforce Equity Market Resilience

What’s the Conjecture?

The media stories surrounding the UST 10-year yield have centered on Treasury Secretary Bessent implementing a policy whereby future coupon auction sizes are reallocated from longer-term maturities to shorter-dated issues. In other words, issue less in ten-year notes and instead increase auction sizes for a two-year note. The goal is to lessen the burden on the 10-year and potentially bring down its yield level or, at worst, place a ‘cap’ on any increase.

Feasibility?

Unfortunately, when the U.S. is running just under $2 billion in budget deficits, the Treasury has rather limited options with debt management strategies. In other words, it’s ‘all hands on deck.’ This point was underscored by Treasury’s recent borrowing advisory committee minutes where it stated that “nominal coupon auction sizes might next increase in early CY2027” with “Treasury to modify its forward guidance several quarters ahead of such a change.”

Another key point is that Bessent has stated that Treasury would maintain “regular and predictable” offerings of coupon securities in order to safeguard the UST market as a benchmark for stability. A policy pursued with another goal in mind could very well ‘spook’ global investors, who may view it as government manipulation of the yield curve.

Conclusion

While stories may continue to circulate on this front, we believe the more likely path is for Treasury to continue following the ‘regular and predictable’ policy that has been in place for many years. As for the direction of the UST 10-year yield, as is typically the case, the primary driver will remain upcoming employment and inflation data, with Treasury supply either adding to, or taking away from, the existing trend.

Kevin serves as the Head of Investment and Fixed Income Strategy.

Maggie Lucier, Senior Associate, Investment Strategy

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.9473, or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

© 2026 WisdomTree, Inc. All Rights Reserved.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.