Energy security and climate policy are increasingly inseparable. Clean technology suppliers benefit from powerful structural tailwinds but also face cyclical risks tied to overcapacity and policy shifts. Meanwhile, fossil fuel exposure carries geopolitical risk and sensitivity to price swings, even when near term demand remains firm.

Case in point: Germany was an early leader in renewable energy, but its continued reliance on Russian gas left it exposed when supplies were cut following Russia’s 2022 invasion of Ukraine. Its economy has lagged the EU since.

More recently, oil price shocks from the conflict in Iran are rippling through global economies. Even if temporary, such disruptions can continue to reprice risks across energy markets and create lasting inflationary pressure. In our view, conflict in the Middle East underscores how dependence on fossil fuels can expose existing vulnerabilities when geopolitics intervene.

Geopolitical Footprints in Renewable Energy

We think renewable energy is well positioned to meet geopolitical challenges and opportunities. Globally, renewable energy deployment continues to grow, hitting a record $2 trillion in 2025.

Renewable assets require higher up-front capital, making financing conditions, interest rates and policy certainty critical. Throughout Africa, for example, the cost of financing projects comprises the lion’s share of electricity costs generated from wind and solar, while in North America the up-front capital cost of building those assets is the dominant driver.

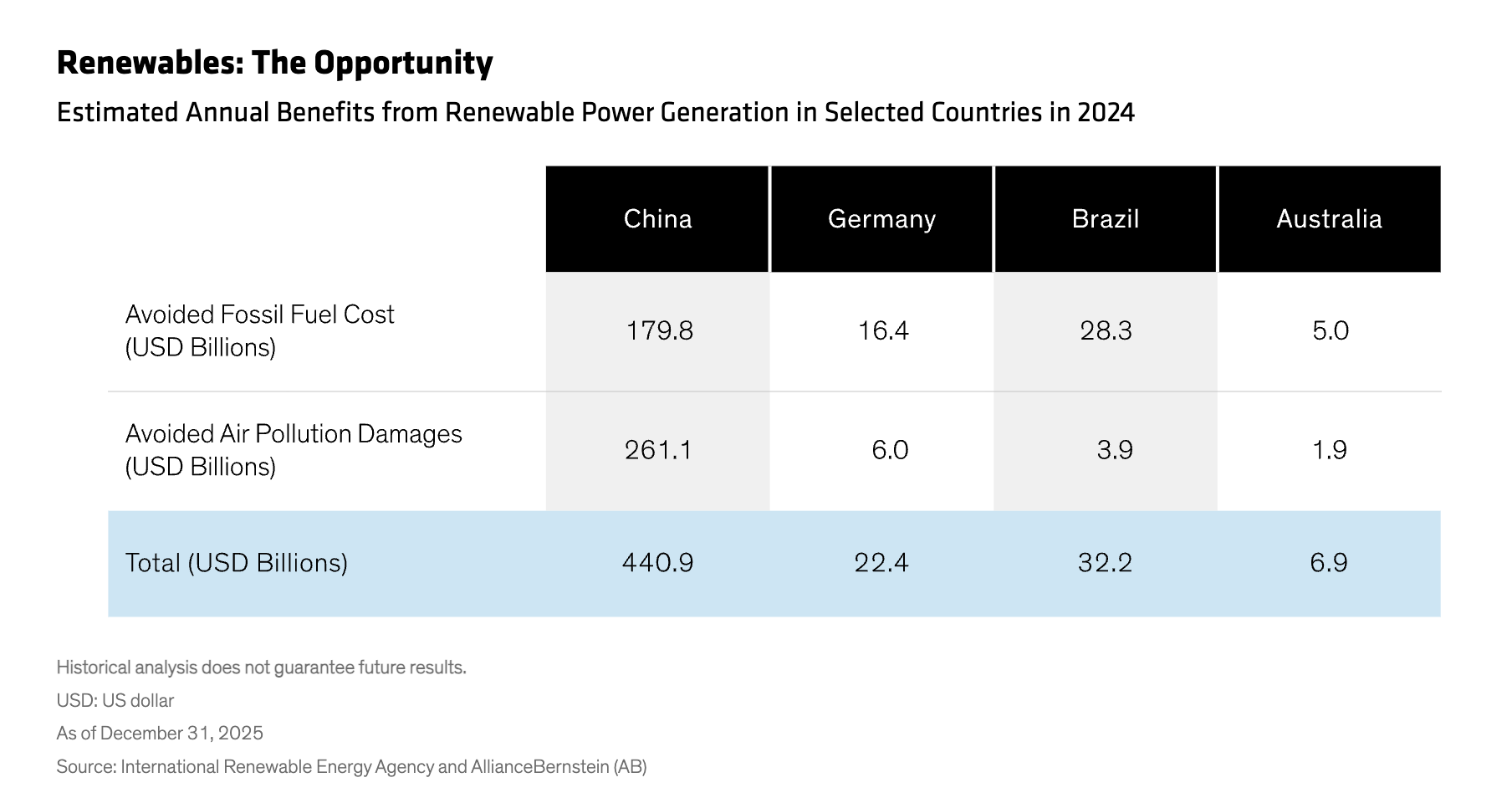

Once built and paid for, however, renewable assets incur minimal operating costs and fuel-price risk. Cost avoidance also factors into renewable energy’s bottom line. China, for example, avoided $441 billion in fossil fuel burning and pollution damage costs in 2024 (Display).

China leads in renewables spending, channeling $600 billion in 2025 to low-carbon technologies such as solar photovoltaics (PV) and electric vehicle manufacturing—about 10% of GDP. In fact, China accounted for at least 70% of combined global clean energy capacity in 2024, according to a BloombergNEF report. It’s also now the world’s largest EV maker, recently surpassing Tesla.

This is not by chance but through policy. In 2014, China laid the blueprint to transform its energy system, prioritizing renewables for state support to reduce import dependence, grow competitiveness and build technological leadership. Though mostly successful, China’s policies unintentionally created overproduction in areas such as solar panels, where a supply glut, global price collapse and layoffs underscore the need for greater policy flexibility.

The Cost Curve Can Matter More than Politics

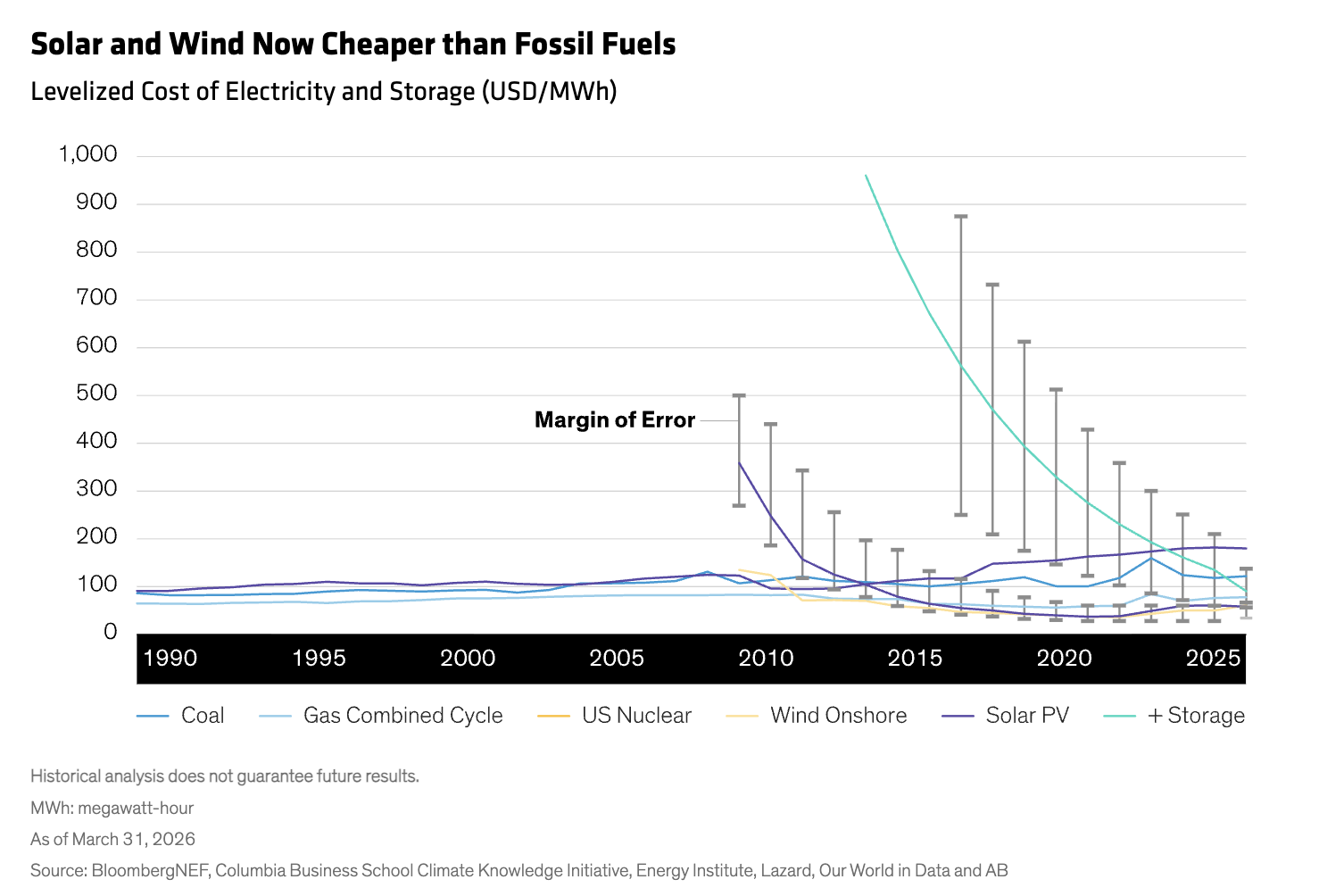

While the cost of coal-generated electricity has barely changed in decades, solar power, wind and batteries (storage) have seen dramatic and sustained cost declines. For example, solar power—prohibitively expensive 40 years ago—is now the cheapest source of electricity (Display). Battery costs also continue to fall sharply due to improvements in technology and economies of scale.

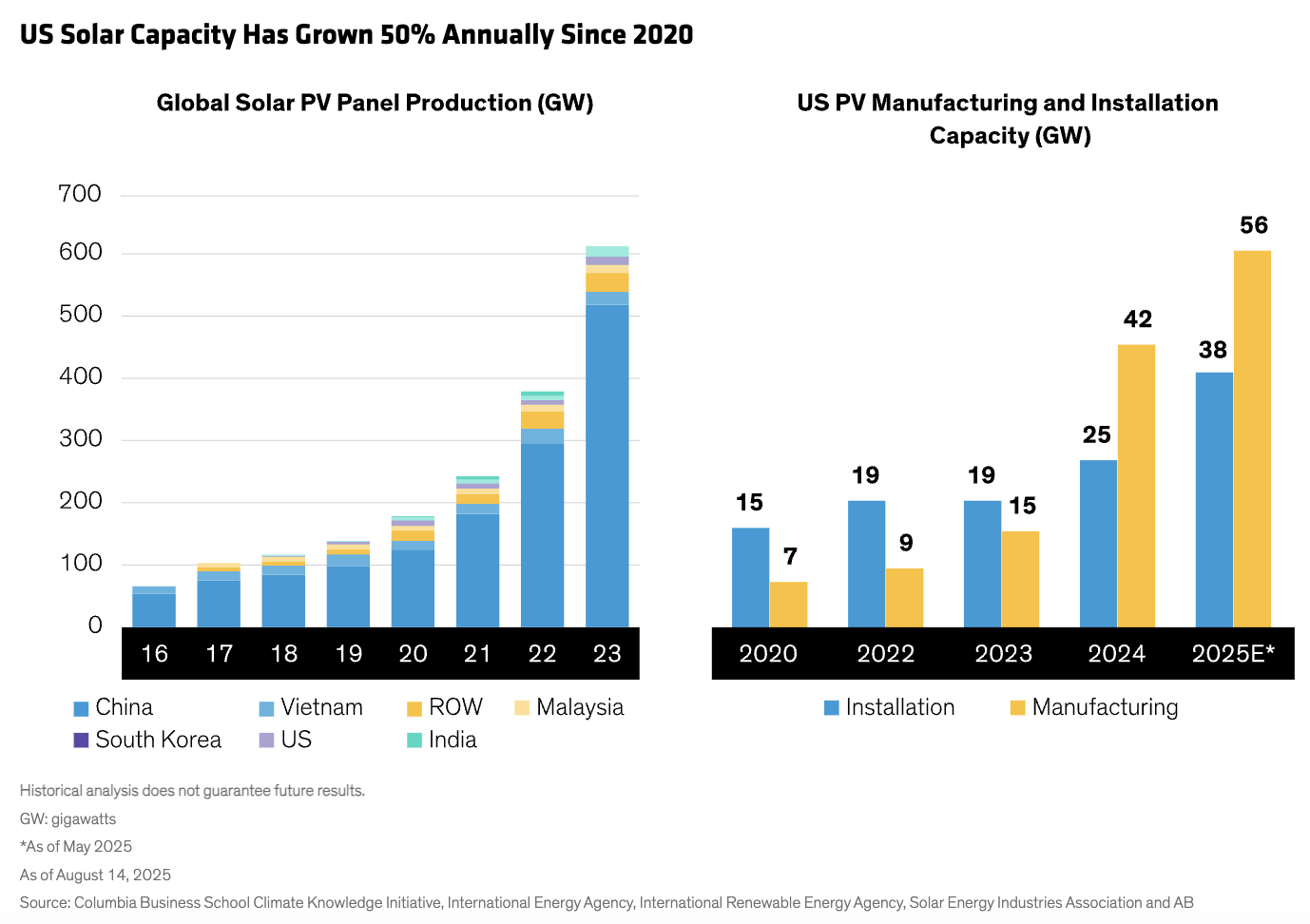

This dynamic helps explain why renewable deployment can gain ground even where climate policy ambitions are lacking. For example, substantial subsidies from the Inflation Reduction Act (IRA) of 2022 accelerated US solar energy production for several years, leading to a 50% annual growth rate and even higher leaps in some states (Display).

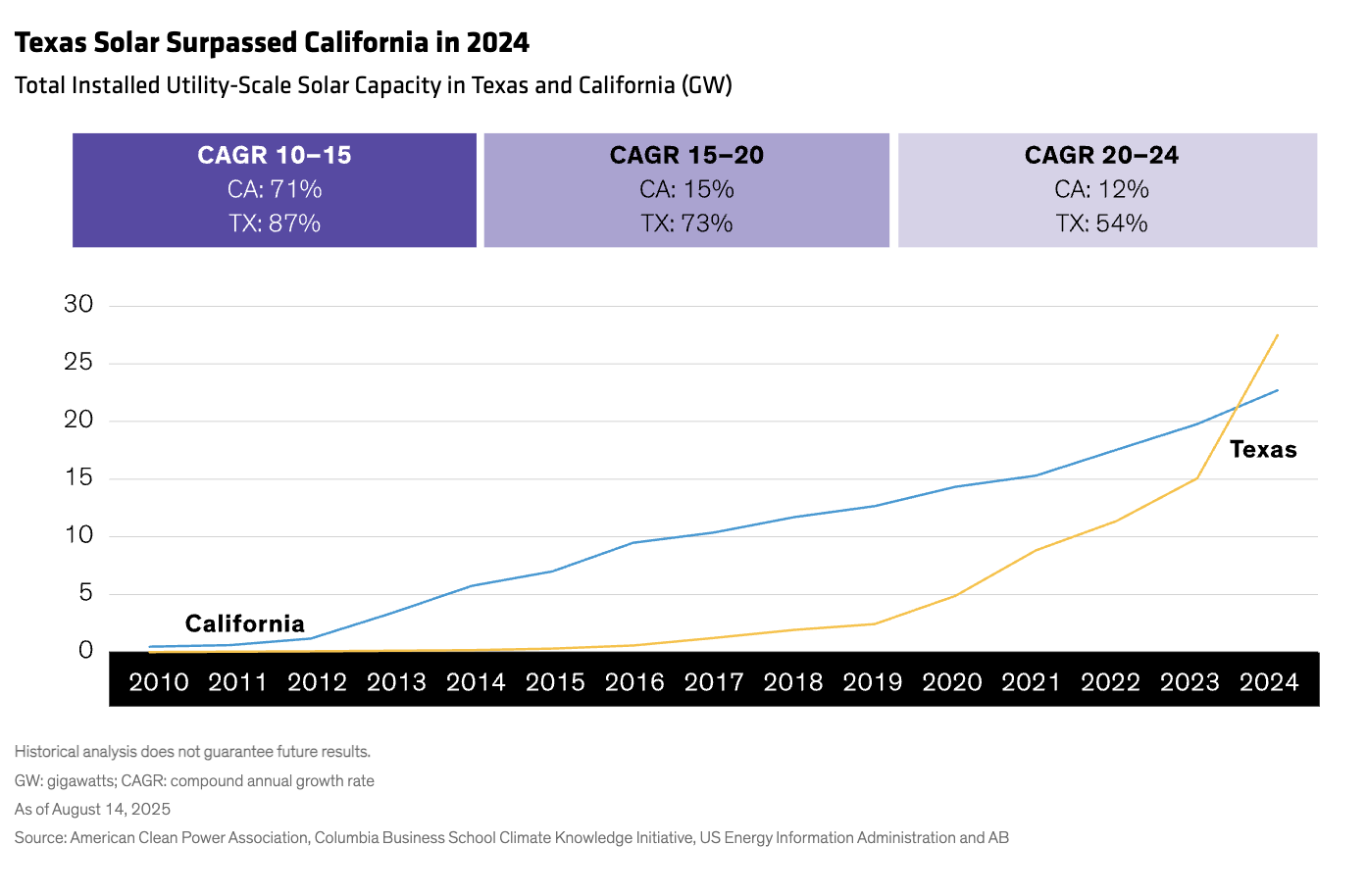

Texas, with relatively little state-level climate policy, surpassed even California in solar PV installations in 2024 (Display). But the surge reflects looser state policies that let installers benefit directly from IRA subsidies rather than environmental considerations alone.

Policy support can be reversed. The US One Big Beautiful Bill Act of 2025, for instance, tightened solar and wind power incentives, while maintaining other subsidies for low-carbon technologies like nuclear and geothermal.

Tariffs are another policy tool with two-sided consequences for renewable energy markets. US levies on renewable equipment may help support domestic production. But US expertise and independence in this area lag competitors and will require years of substantial investment in technology and labor. Until it can fill the supply chain domestically, the US will be challenged to manage costs, particularly when inputs include tariff-inflated components.

Investment Implications of Climate Geopolitics

For investors, the rise of climate geopolitics does not produce simple winners and losers. Rather, it rewards adaptability. Utilities with access to low cost clean power and grid investment opportunities may benefit significantly from rising demand in our analysis. Meanwhile, energy intensive industries face pressure, but those that invest early in efficiency and cleaner processes may improve long term competitiveness.

We see strong renewable opportunities among suppliers of solar panels, wind turbines and grid-level equipment. Many are based in emerging markets, including China, South Korea, Taiwan and Southeast Asia.

While policy can accelerate or slow clean energy adoption, cost curves—not politics alone—are likely to determine long term direction. The key is not to predict politics but to understand how regulation, commodity cycles, energy demand and technology costs interact across regions and industries. Climate geopolitics are reshaping markets unevenly—but decisively. For investors, the cost of ignoring that shift can be sudden and severe.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

References to specific securities discussed are for illustrative purposes only and should not to be considered recommendations by AllianceBernstein L.P. It should not be assumed that investments in the securities mentioned have necessarily been or will necessarily be profitable.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.