The U.S. economy appears resilient, judging from key economic measures. AI-driven capex continues to power investment, support equity markets, and sustain a wealth effect that has propped up consumption. Real GDP growth remains positive. Private sector balance sheets are in generally good condition and many higher income and wealthy households have benefited from equity markets gains.

However, fragilities are increasing, especially as U.S. households must now absorb another meaningful hit to their purchasing power, on top various other drags on real income growth. Tariffs, higher energy prices, slowing wage growth, and other factors have driven a sharp drop in real disposable personal income.

Usually, we would expect households to smooth through temporary changes in current income. However, households have been dealing with a series of shocks that have reduced the savings rate to historically low levels and risk denting expectations for future real income growth. Furthermore, AI is a new source of uncertainty for many workers.

This means real consumption growth, at some point, could catch down to real income reality. And if consumption slows, the effect could reverberate through the economy.

Income and consumption: a complex link

Historical data and economic theory point to a complicated relationship between income and consumption.

In the late 1950s, economist and future Nobel laureate Milton Friedman developed the permanent income hypothesis (PIH). It argues that consumption is determined not by current income alone, but by expected lifetime income. According to the PIH, temporary income shocks shouldn’t move spending much. If households believe the income change is transitory (e.g., a one-off energy spike), they tend to smooth through it; if they think it’s persistent or permanent (e.g., structural labor market weakening), they tend to lower their consumption.

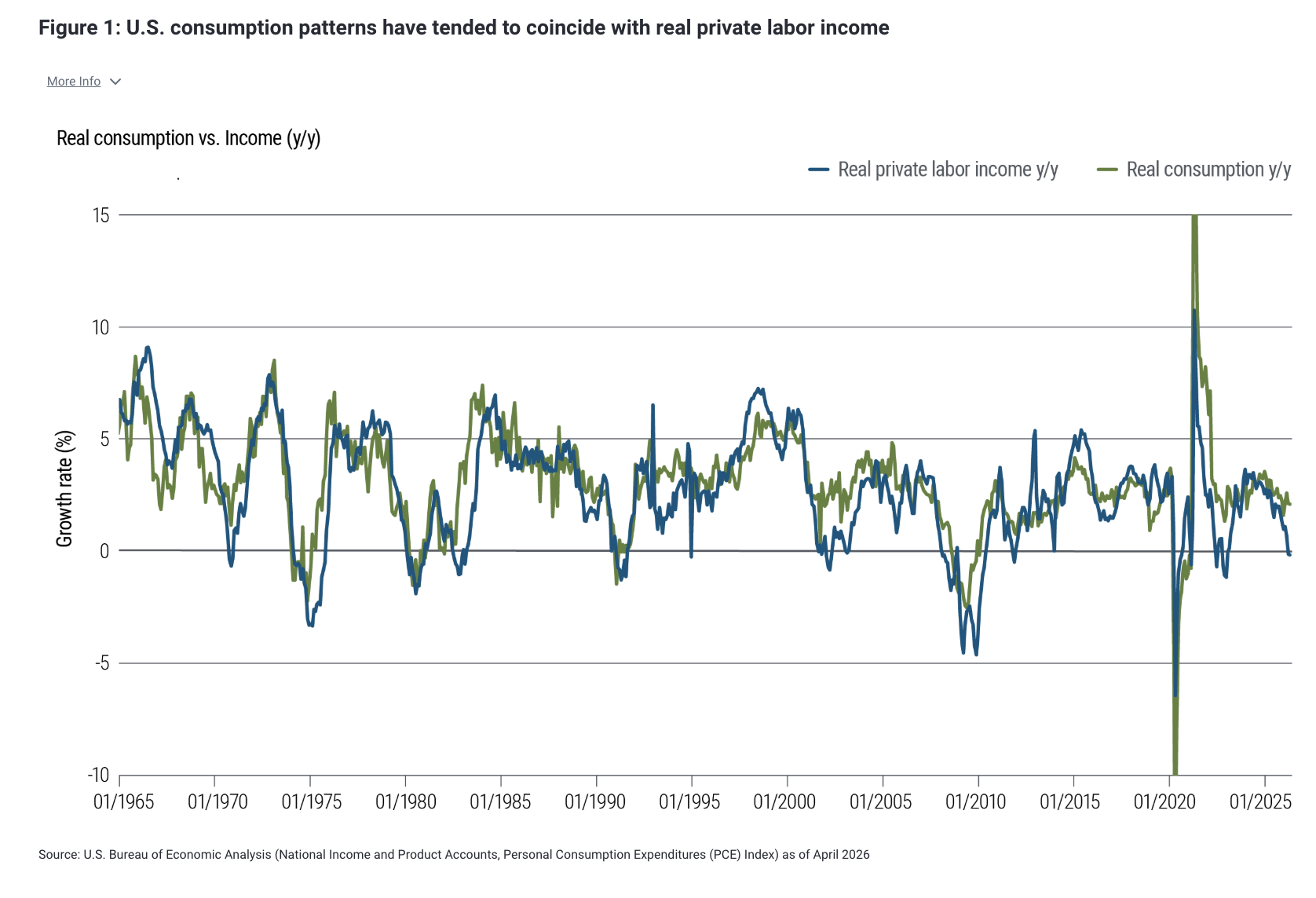

Although the PIH predicts that consumption responds only to unexpected changes or news about permanent income, historical data have consistently shown that consumption seems to respond too sharply to predictable changes in current income – an effect termed “excess sensitivity.” Historically real income and consumption have tracked closely (See Figure 1)

Later research has found fundamental reasons for this excess sensitivity. Specifically, the population of households includes some portion living paycheck to paycheck or with precarious financial situations – and these households lack the means to smooth through periods of real income shocks even if they believe them to be temporary.

Mathematically, consumption can hold up for a time when income weakens – through spending down savings, wealth generation, or temporary cash flow boosts but without a constant source of real income households can’t sustain consumption after these buffers are exhausted.

Other research suggests uncertainty also plays an important role. Specifically, savings and consumption decisions are based not only on expectations of lifetime income, but also on risks. A more risk-averse household might save extra as a buffer against uncertainty. Or as uncertainty rises, they save more – even if their expectations for permanent income haven’t changed.

Read more: AOR Update: Resilience

When shocks compound, expectations shift and spending shrinks

Real incomes are now contracting, due to a series of shocks that have compounded. Tariff pass-through, higher energy prices and slowing nominal wage growth have coincided with changes in household tax rates, social security, and government food assistance programs, and one time farm income subsidies. Immigration and other policy changes have also played a role.

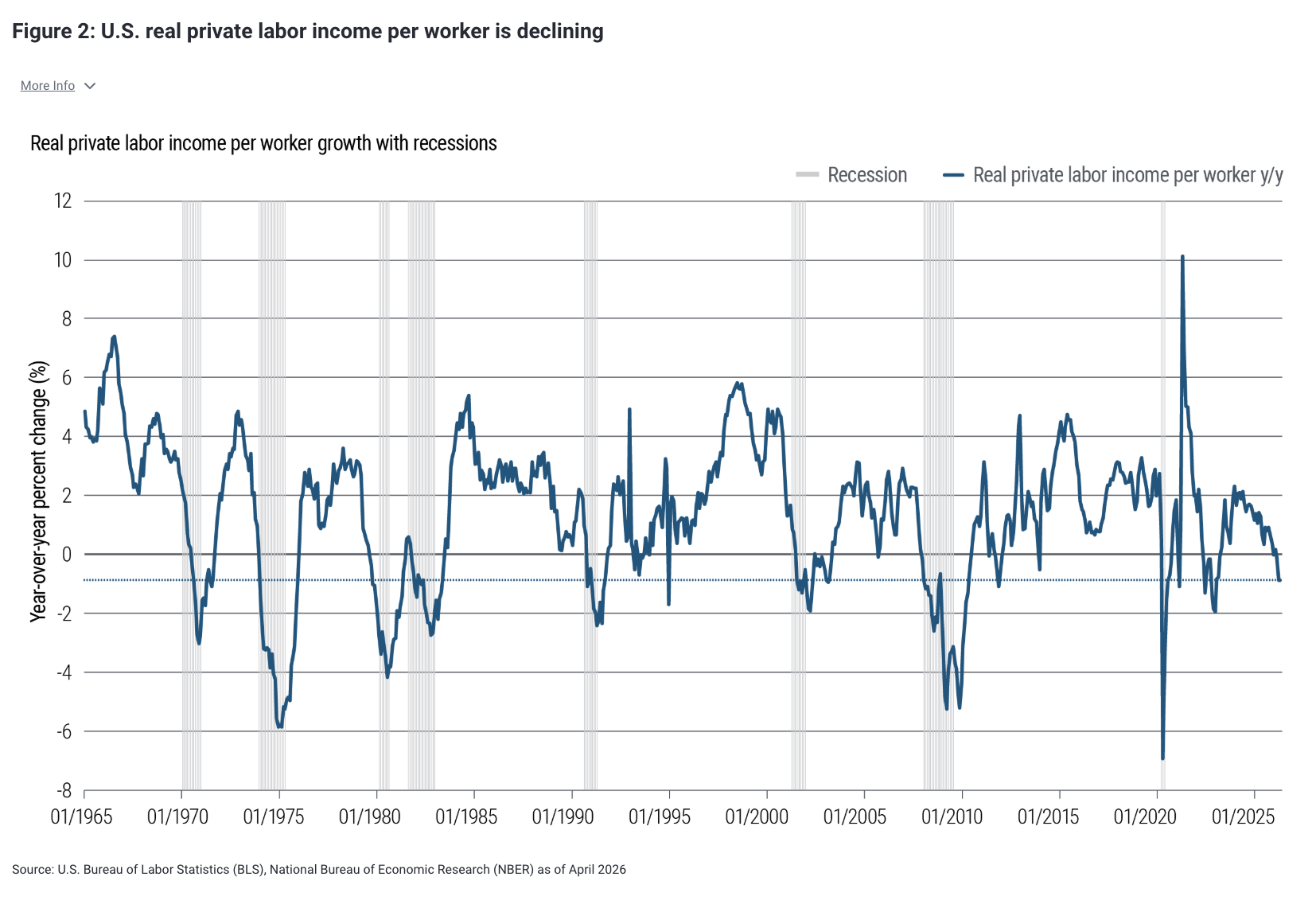

As of April, real disposable personal income, which measures after-tax income from both labor and non-labor sources was down 1.1% from a year earlier. Stripping out the impact of policy and immigration policies, a “core” measure of income – real labor income per available worker (which doesn’t include policy effects) – contracted 0.9% versus the previous year as of April, according to the U.S. Bureau of Labor Statistics. That’s a pace not usually seen outside of recession (see Figure 2).

Since the pandemic, U.S. consumption growth has generally outpaced real income growth as greater wealth has coincided with a lower average saving rate. However, looking ahead, we see good reasons why consumption may slow.

First, already historically low household savings rates suggesting household buffers are more limited. The personal saving rate fell to 2.6% of disposable income as of April, according to the BEA. Outside of the period leading up to the global financial crisis and the 2022 energy shock, the saving rate has rarely been this low in data going back to 1960. The only other period of sustained low household savings rate was the 2004-2006 period when housing debt was rapidly increasing.

Greater wealth likely explains at least some of the decline in the savings rate over the last few years, but there are limits to how much further it can fall – particularly since wealth gains are concentrated among higher-income households while the energy and tariff hit falls disproportionately on lower-income consumers with limited resources and the highest marginal propensity to spend.

Second, the income shock is not a single temporary factor, but rather a series of shocks over the past few years that could be permanently altering expectations of future real earnings. Labor market conditions are the primary channel through which households form income expectations. And although we’ve more recently seen encouraging signs that labor market activity is stabilizing or even picking up over the last few years, a growing degree of labor market slack has been evident across indicators. The ratio of job openings to the number of unemployed workers is hovering around 1.0 as of April, according to the BLS – historically the vacancies to unemployment (V/U) ratio doesn’t tend to fall below 1 outside of recessions. The quits rate is below pre-pandemic levels, and consumer surveys of labor market conditions – including the Conference Board’s “jobs plentiful” versus “jobs hard to get” measure – have continued to gradually decline, suggesting workers feel less confident about outside options and labor market conditions more generally. Measures of wage inflation have also gradually declined, especially for lower paying jobs.

Third, relevant polling suggests that the rapid pace of AI technological progress and implementation is increasing uncertainty around the outlook for future incomes. According to Pew Research, about a third of workers say AI use will lead to fewer job opportunities for them in the long run. A recent yougov.com poll found similar sentiments. More Americans are pessimistic than optimistic about AI's long-term effects, with young adults more likely to worry that AI will replace jobs they depend upon.

Economic resilience has limits

The U.S. economy appears resilient. Private sector balance sheets are broadly healthy, higher-income households have benefited from strong equity markets, and AI-driven investment continues to support headline growth. But resilience is not the same as durability.

The real income data are sending an increasingly clear signal: Household purchasing power is contracting, at a time of an already historically low savings rate, and the temporary supports that have bridged the gap between weakening income and steady spending – such as One Big Beautiful Bill Act (OBBBA) tax refunds – are fading.

The deeper risk is that households will start to believe that the forces currently squeezing real income are more persistent than transitory. Friedman’s permanent income hypothesis tells us that what matters most is not whether income falls today, but whether households believe it will recover. Right now, the combination of a series of real income shocks over the last few years, and early signs of AI-related labor market disruption creates a plausible case that households may start to revise those expectations lower. If they do, consumption will follow – not because of a single shock, but because the accumulation of drags has quietly eroded the foundation.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0602-5545721

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

More Mutual Funds Topics >