Insurance investors face a broader opportunity set than ever across public and private credit—from corporate lending to asset-based finance. But those investments come in many forms. In our view, a all-encompassing approach can better assess relative value, pivot to new avenues and align investments with portfolio, liability and regulatory considerations.

Security Innovation Is a Constant in Financial Markets

Innovation in corporate and asset-based finance is hardly a new concept—the cutting edge continues to sharpen itself. In the 1990s, future music royalties of musician David Bowie were converted into asset-backed securities. The late 2000s saw the emergence of securitizations backed by loans to time-share residents.

More recently, securities have been backed by revenues from leased space in data centers or digital-infrastructure operations. Financial markets continue to develop new security structures as a growing number of companies and banks see the efficiency of tapping securitized and private markets to raise capital and right-size balance sheets.

For insurance investors today, the range of opportunities in collateral is wide: corporations, homes and offices, consumer goods and services, hard assets and financial assets. So are the access points: public and private securities, whole loans, warehouse lending and securitizations.

New Opportunities Often Have “Expiration Dates”

But it can be a challenge for investors to keep their arms around such a sprawling opportunity set, with new securities coming to market regularly and with valuations shifting constantly. Such a complex landscape could strain a more rigid approach focused only on “known” asset classes or sectors.

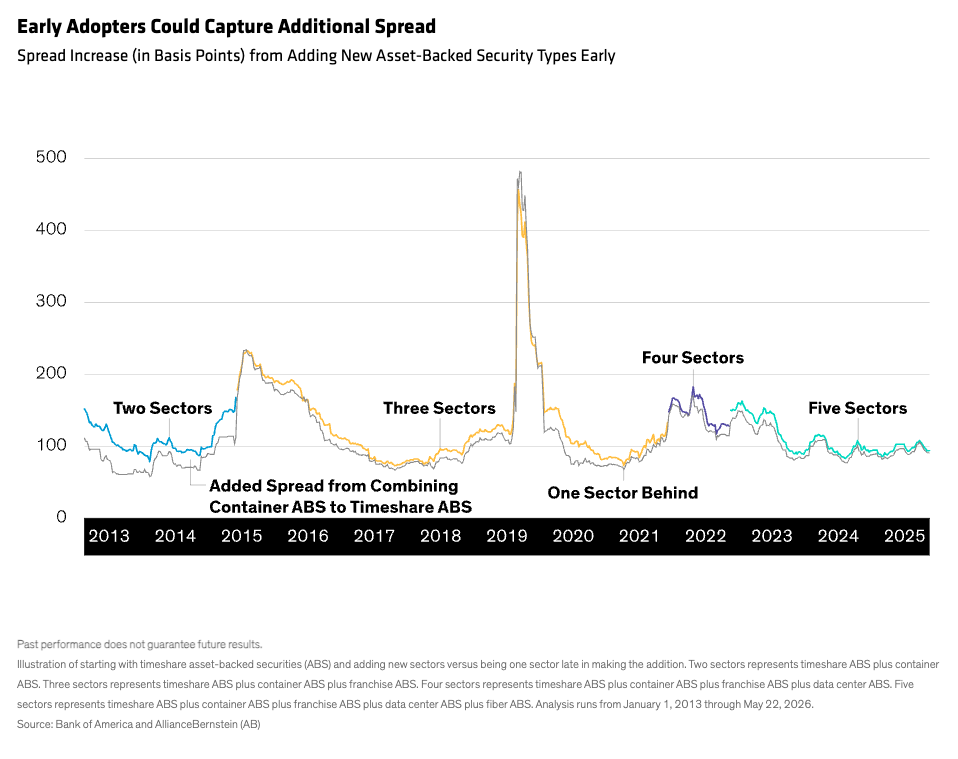

There’s a case to be made that early adopters of new asset types have been able to access higher yields and spreads (Display). That’s because newer sectors have tended to trade at larger spreads before subsequent investors discover them and bring more capital to bear. If investors can’t pivot into them quickly enough, these investments could be a missed opportunity.

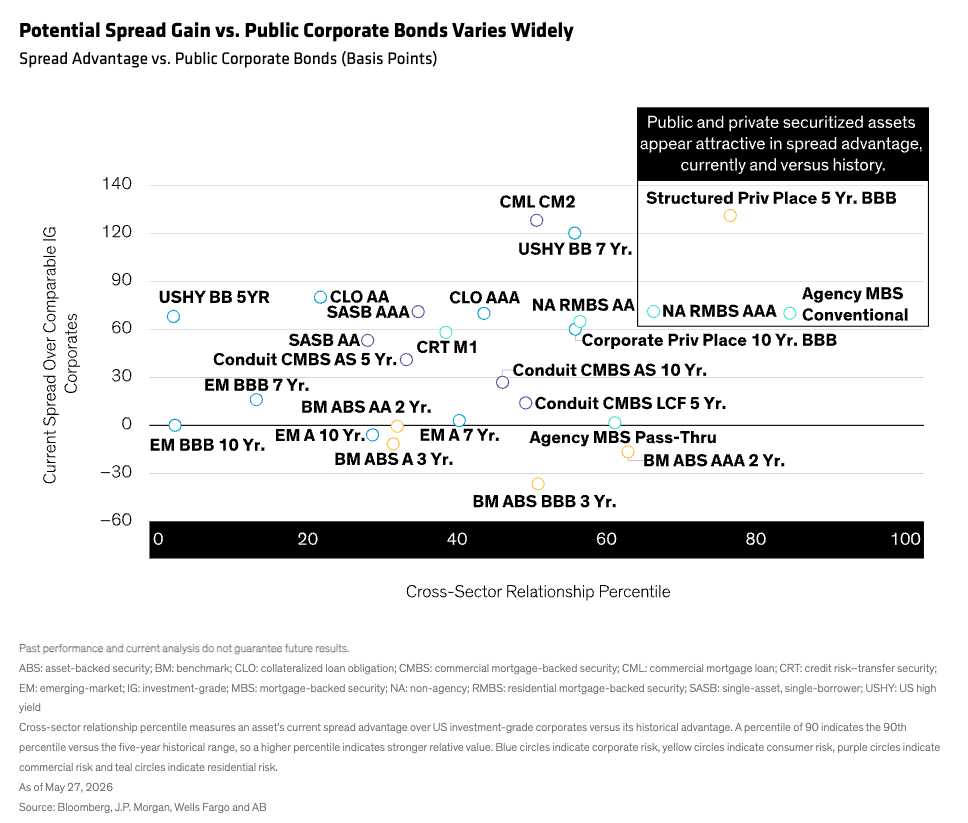

More broadly, spreads vary quite a bit among public and private securitized assets. Private asset-backed securities have seemed particularly attractive (Display), offering an average of about 150 basis points of yield over public corporate bonds. But spreads could be as low as 120 or as high as 190 or more, depending on the security. That puts a premium on assessing relative value accurately and quickly.

Different Fundamentals Require Different Skills

Assessing the macroeconomic and fundamental factors that define opportunities and risks in an expansive universe requires multidimensional capabilities. Aviation leasing and timeshare asset-backed securitizations, for instance, both fall under private credit but with very different drivers.

Success in aviation leasing requires a deep understanding of aviation market dynamics, the valuation of different aircraft models and vintages, technical aspects of aircraft maintenance, and how global economic conditions influence airlines’ profitability and the volume of air travel demand.

On the other hand, analyzing timeshare asset-backed securitizations requires a seasoned eye to interpret the dynamics of real estate and hospitality markets; how factors such as location, amenities, and market trends affect property valuations; and the legal framework that governs timeshare sales.

One Size Doesn’t Fit All for Insurance Investors

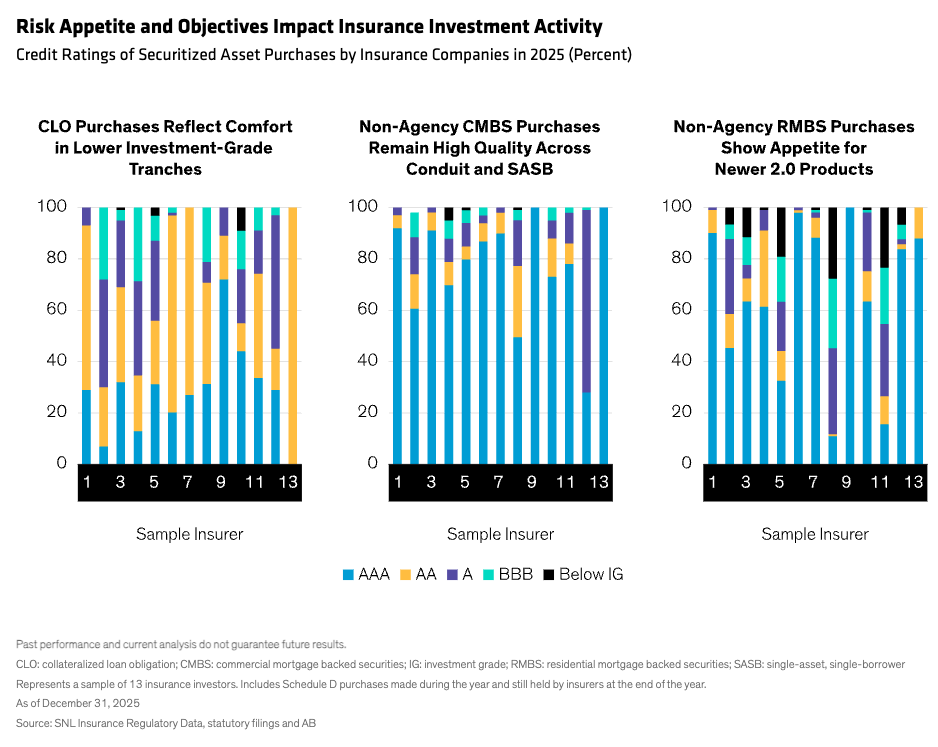

There’s a misperception that insurance portfolios include the same asset types and allocations. But recent data suggest otherwise—even in the same industry segment. For instance, 2025 purchase data across a group of life insurance firms illustrates how wide securitized preferences can range (Display).

Private credit preferences can diverge, too, depending on insurers’ specific needs when it comes to liabilities and investment guidelines.

For insurers seeking long-term assets to match long-term liabilities, investing in renewable energy infrastructure may help, and financing is increasingly coming from private lenders. Many investments have longer maturities in the 20-year range; spreads are modest, but may be appealing where spread assets are more scarce. Insurers with shorter-duration liabilities, on the other hand, must consider the trade-off between return potential and diversification.

From a regulatory standpoint, some infrastructure investment—particularly in Europe—may bring lower capital requirements. Regulatory regimes dictate requirements for insurers, too. Some assets, such as home improvement loans, are actually consumer loans and not admittable assets as per the National Association of Insurance Commissioners. To check the “rules” box, insurers must access these assets through specific structures.

The bottom line: insurance investors need tailored investments, not off-the-rack.

Casting a Broad Net Around an Ever-Growing Field of Opportunities

Insurers have been pouring sizable amounts of capital into an increasingly diverse marketplace. Traditionally, this involves allocating to distinct market segments. Governance committees assemble a stable of managers covering each segment and manage the overall mix. Periodically, they revisit the composition, review manager track records, assess overlapping risks, adjust exposures and consider adding new segments. For those willing to invest the time and expense, this may be a useful approach.

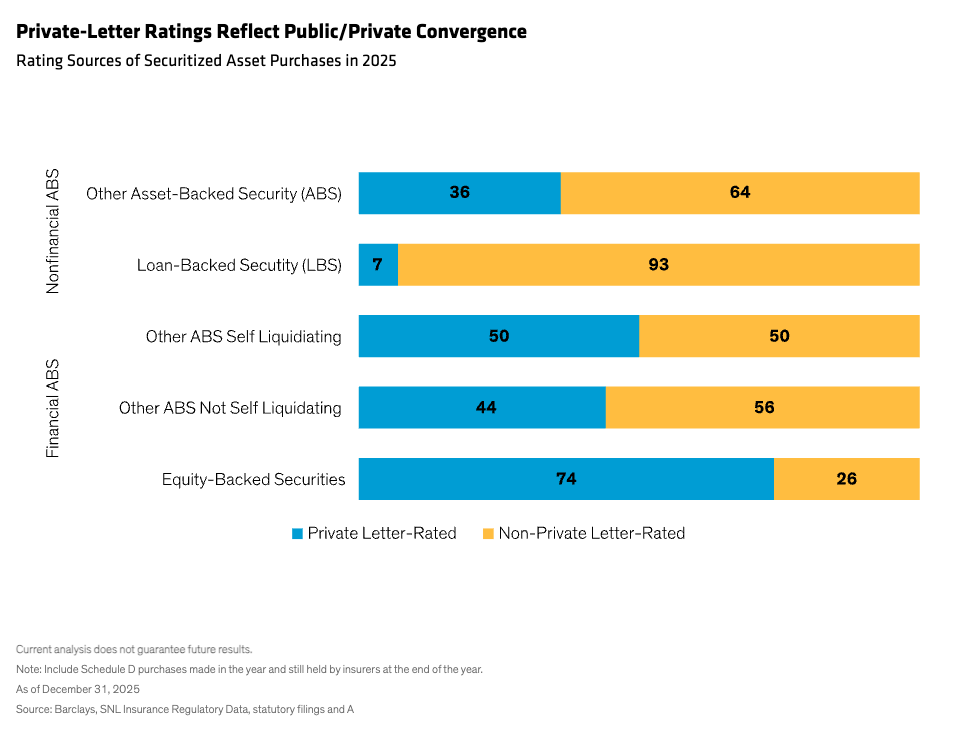

But we see another way—one holistic allocation embracing all segments of public and private markets. Sourcing and origination, research, credit underwriting and due diligence winnow the broad universe down to an investable one. This set is then assessed for relative value through an insurance lens in real time and evaluated for alignment with guidelines. Investments are managed at the individual deal and portfolio levels. As public and private markets converge (Display), it’s critical to evaluate wide-ranging underlying risks and relative value this way—no matter the type of investment.

This approach requires a broad skill set and capabilities, but we think it’s a promising way to tackle an investment problem with many moving parts. Opportunities come in different shapes and sizes and the playing field shifts quickly, requiring nimbleness to capture opportunities early while monitoring risks.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More Fixed Income Topics >