Weekly Economic Snapshot: Strong Economy but Worried Consumers

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLast week’s economic data presented a sharp contradiction between a resilient U.S. economy and increasingly concerned American households. The S&P 500 fell for most of last week but recovered some of those losses following Friday’s inflation report. A final estimate showed the U.S. economy posted a stronger than expected rebound in the second quarter, primarily driven by an increase in consumer spending. However, despite this strength, consumer sentiment dropped to a four-month low as households grew more concerned about the economic outlook.

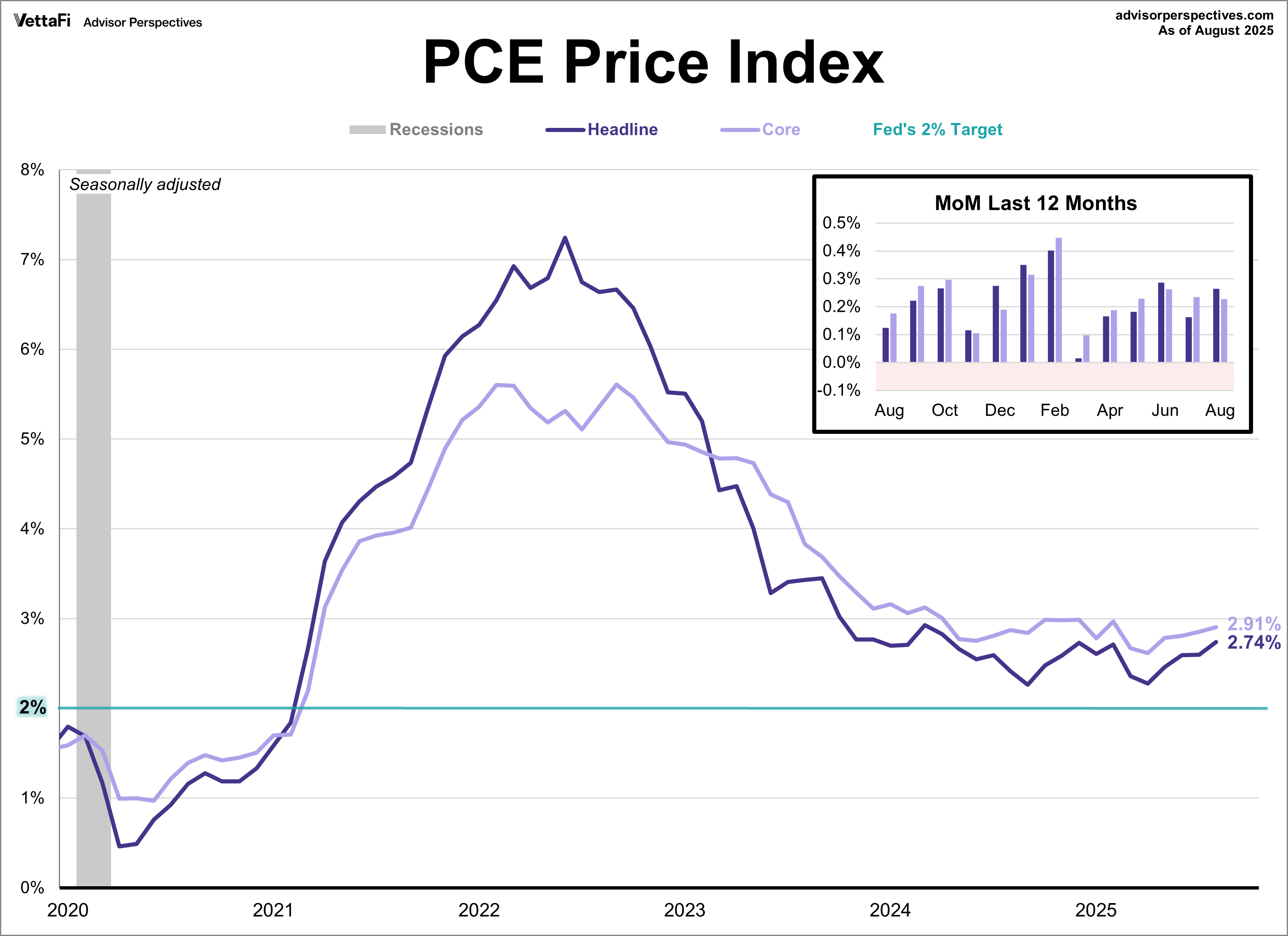

PCE Price Index

The Federal Reserve’s preferred inflation gauge reached its highest level in six months as it edged further away from the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.9% year-over-year in August. This was consistent with the forecast and marked a slight pickup from July. Meanwhile, the headline index jumped to its highest level since April 2024, rising 2.7%, as expected. On a monthly basis, core prices rose by 0.2% and headline prices rose by 0.3%, both as expected.

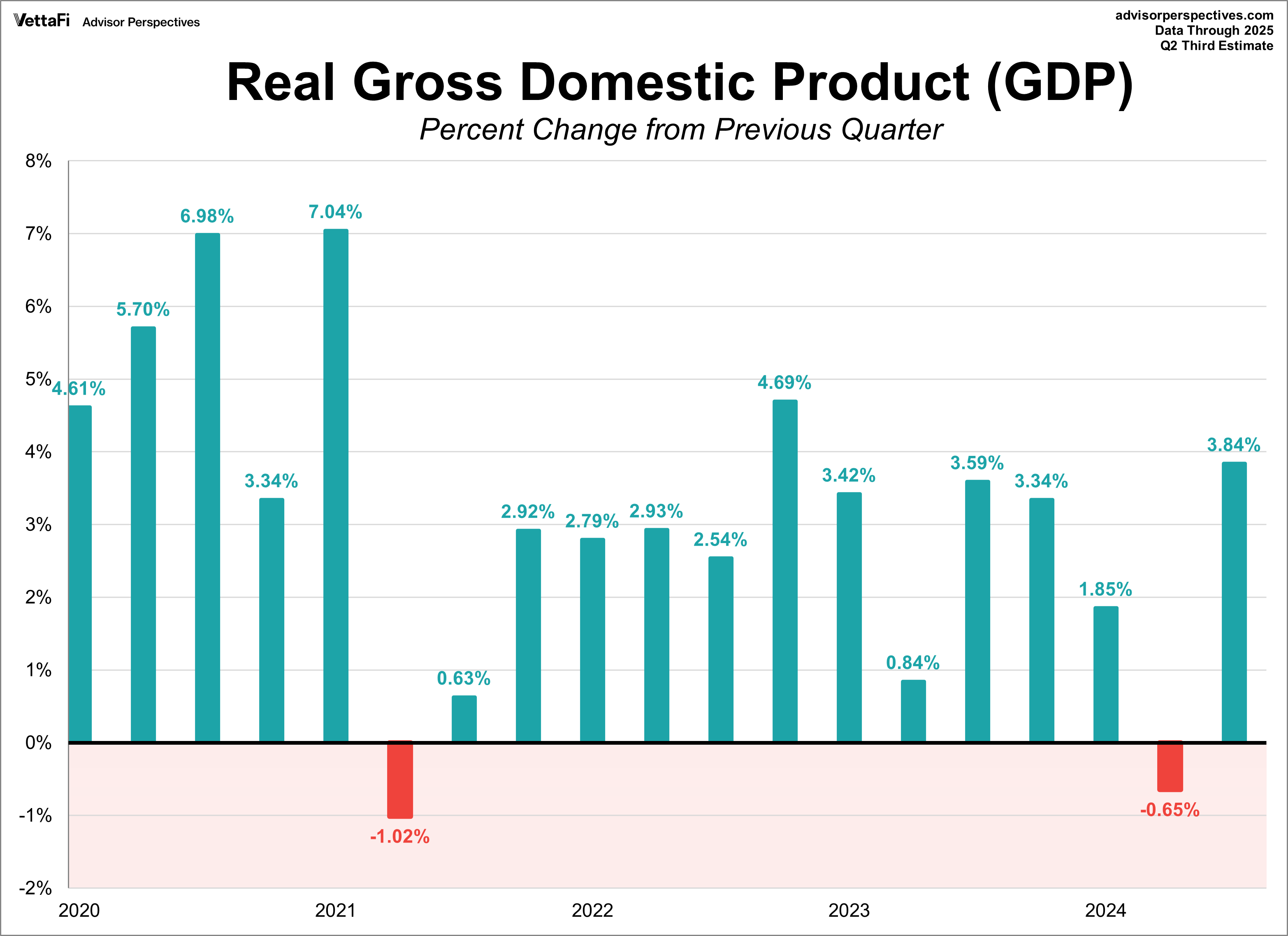

Gross Domestic Product (GDP)

According to the third estimate, the U.S. economy posted a stronger than expected rebound in the second quarter. Real GDP, the inflation-adjusted measure of all goods and services produced, increased at an annual rate of 3.8% from April to June. This marks a significant turnaround from the first quarter’s 0.6% contraction and surpassed the 3.3% forecast from last month’s estimate. The expansion was primarily driven by a decline in imports and an increase in consumer spending, although these gains were partially offset by a decline in business investment and a fall in exports.

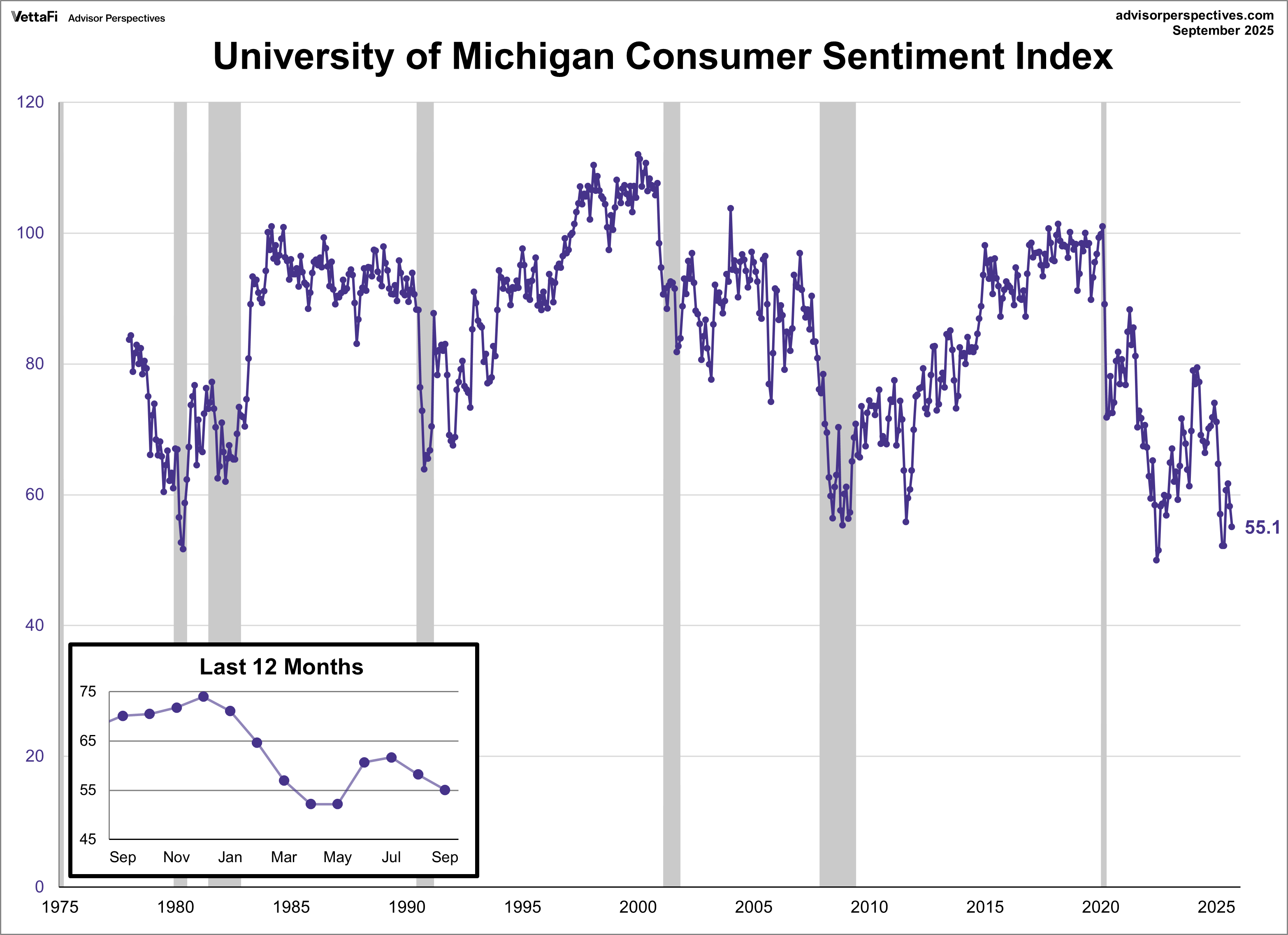

University of Michigan Consumer Sentiment Index

Consumer sentiment fell for a second consecutive month in September, reaching its lowest level since May. The University of Michigan Consumer Sentiment Index dropped by more than 5.0% to 55.1 this month, coming in below the forecast of 55.4.

The index’s deterioration was broad-based, impacting nearly all demographic groups. The notable exception was among consumers with large stock holdings, whose sentiment remained steady. Additionally, all five components of the index worsened this month as mounting economic concerns took hold, particularly around the labor market and personal finances.

Inflation expectations for the near term eased slightly to 4.7% from 4.8% for the year ahead. Meanwhile long term expectations heated up for a second straight month, jumping from 3.5% to 3.7% for the five-year outlook.

Market Reactions

The S&P 500 notched a new record high last week but mid-week setbacks led to the index’s first weekly loss in almost a month. The index ultimately posted a loss of 0.3% for the week. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 0.3% last week. Meanwhile, the S&P Equal Weight Index was up 0.1% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 0.3%.

The 10-year Treasury yield finished the week at 4.20%, while the 2-year note finished at 3.63%.

The CME FedWatch Tool currently shows a 90% likelihood that the Fed will cut rates by 25 basis points at their next meeting. Markets are also pricing in another 25 basis point cut at the December meeting and two additional cuts in 2026.

Economic Data in the Week Ahead

The week ahead will deliver a comprehensive view of the labor market and broader economic activity. The most highly anticipated data will be the BLS Employment Report on Friday, preceded by the ADP Employment Report, the JOLTS Report, and weekly jobless claims, all of which will provide insight into labor market health. A comprehensive look at factory and service sector health will be provided by the key ISM Manufacturing and Services PMIs, complemented by the S&P Global PMIs and regional reports like the Dallas Fed Manufacturing Index and the Chicago PMI. Finally, data on consumer sentiment and the housing market will round out the week with the release of the Conference Board’s Consumer Confidence Index, the S&P Case-Shiller Home Price Index, and Pending Home Sales.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All